It is tempting today to write about the relative price performance of low-growth (let’s call them ‘value’) versus high-growth companies, defensives versus cyclicals, the stellar price performance of the so-called bond proxies, or how devastatingly successful a momentum-based investment strategy has been over the past 10 years. But commentary on these topics seems to have been particularly well-trodden ground of late and I’m not sure we can add much insight. Plus, we were tempted to write about these last year, which reinforces how little competitive advantage we have in picking trends.

It is tempting today to write about the relative price performance of low-growth (let’s call them ‘value’) versus high-growth companies, defensives versus cyclicals, the stellar price performance of the so-called bond proxies, or how devastatingly successful a momentum-based investment strategy has been over the past 10 years. But commentary on these topics seems to have been particularly well-trodden ground of late and I’m not sure we can add much insight. Plus, we were tempted to write about these last year, which reinforces how little competitive advantage we have in picking trends.

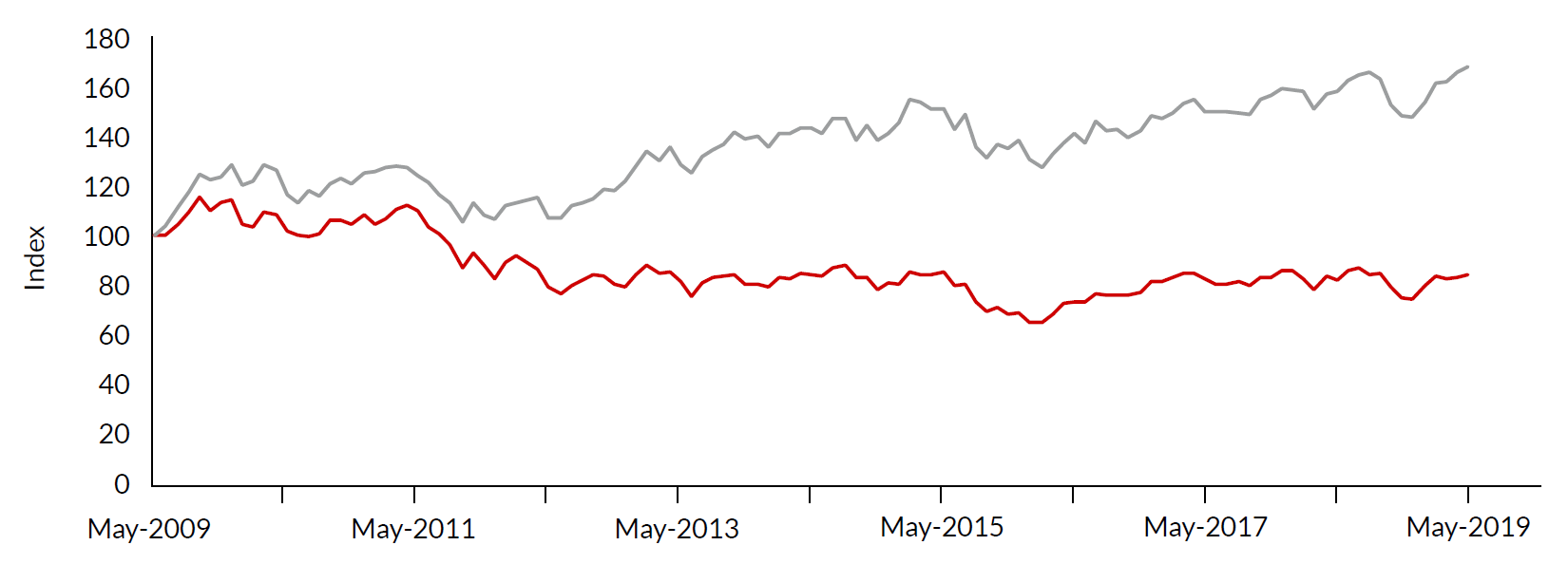

Rather than further analysing these gale-force trends in the market, we continue to focus our efforts on investing in attractively-priced companies. That focus has yielded a portfolio that, if share price is anything to go by, is about as undervalued as it has ever been relative to the broader sharemarket. As Graph 1 shows, a portfolio identical to ours today would have underperformed the sharemarket by 49% had it been initiated ten years ago.

Price, or what you pay, is only part of the story. The other part is the future earnings stream you receive. This is especially important today, given the extent of structural change which has significantly and permanently reduced the earnings outlooks for several companies and industries. A portfolio comprised exclusively of these companies is very unlikely to recover in price terms, given the permanent reduction in its future earnings.

But for the most part, our portfolio consists of cyclically-impacted companies that trade at attractive multiples of depressed earnings and this should help narrow the price gap in Graph 1 considerably.

Graph 1: Our current investment portfolio would have underperformed the market significantly if we had bought those stocks 10 years ago

Source: Allan Gray Australia, Factset, as at 31 May 2019

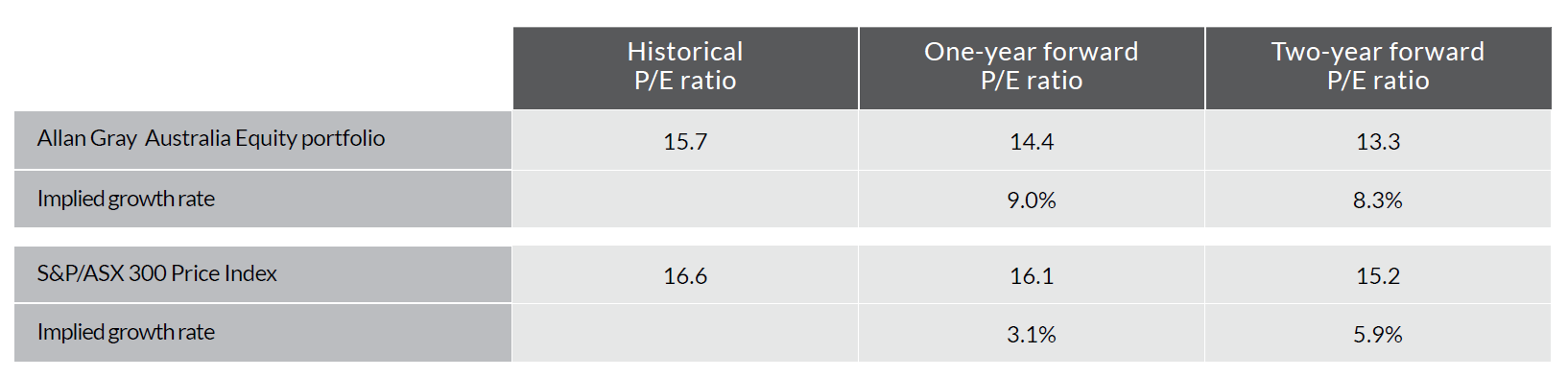

Don’t take our word for it. Table 1 illustrates the view of sell-side analysts. According to them (or ‘market consensus’), our portfolio trades at a discount to the market’s earnings (its price/ earnings or P/E ratio is lower at 15.7 times versus the broader sharemarket’s 16.6 times as at 30 June 2019) and those earnings are expected to grow faster than the market’s.

Table 1: The Allan Gray Australia Equity portfolio trades at a discount to the market’s earnings

Source: Allan Gray Australia, Factset, as at 30 June 2019

It would be fair to question how this is possible. Part of the answer would involve opining on matters alluded to in the first paragraph. Most of the companies we invest in are currently experiencing significant headwinds and their immediate future appears quite bleak. In many instances the investment community may have lost patience. But headwinds can become tailwinds when you least expect it: an unexpected favourable tweet, sudden drought-breaking rains or a less severe recession than people anticipate to name a few. And companies priced for a bleak future make for great investments if the future is only bad.

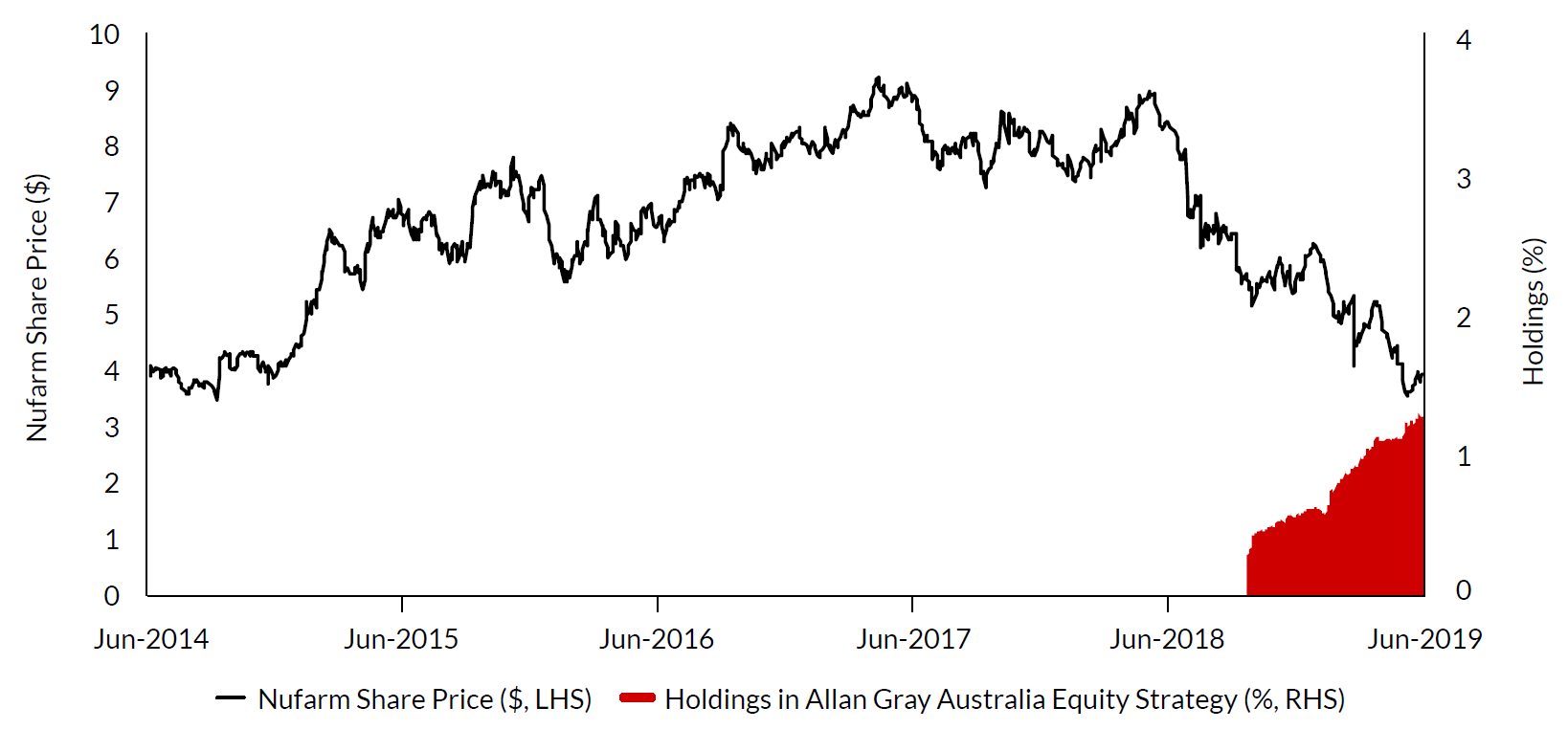

One such company that has been recently added to the portfolio is Nufarm Limited, which finds itself in the middle of a possible cyclical earnings low point, while carrying too much debt. In this extract from the June 2019 Quarterly Commentary below, Dr Suhas Nayak explores the opportunities we see in Nufarm despite the evident risks.

Who is Nufarm?

Nufarm Limited is primarily a formulator and distributor of agricultural chemicals, but it also operates a small seed supply business. Through a number of acquisitions over the years, the company has branched out from its New Zealand beginnings to become one of the largest off-patent agricultural chemical players in the world. Its product range includes herbicides, insecticides and fungicides that keep pests under control and agricultural yields up.

Nufarm Limited is primarily a formulator and distributor of agricultural chemicals, but it also operates a small seed supply business. Through a number of acquisitions over the years, the company has branched out from its New Zealand beginnings to become one of the largest off-patent agricultural chemical players in the world. Its product range includes herbicides, insecticides and fungicides that keep pests under control and agricultural yields up.

Nufarm buys active ingredients from various suppliers (mainly in China), adds some solvents and then sells the formulation to local farmers in Australia, North America, Europe and Brazil. The only active ingredient it manufactures is 2,4-D, a herbicide, which it manufactures in Australia and the UK.

Separately, Nufarm supplies canola, sorghum and sunflower seeds. It also has a promising new seed development program in the late stages of trials and approvals: the omega-3 canola seed, which they claim is the world’s first plant-based source of long-chain omega-3 fatty acids (known for their heart health benefits).

What went wrong for Nufarm…?

The last year has been very difficult for the company, which has resulted in a steep decline in its share price.

Nufarm was riding high when it acquired two European product portfolios in late 2017, an opportunity that came about because of antitrust regulations on the back of consolidation elsewhere in the sector. Despite being partially funded through an equity raising at almost double today’s share price, the acquisition left Nufarm with too much debt if market conditions turned, and turn they did. In Nufarm’s case, this turn was quite sudden and pronounced.

Graph 2: Nufarm share price relative to the share’s weighting in the Allan Gray Australia Equity Strategy

Source: Allan Gray Australia and Datastream. The Allan Gray Australia Equity Strategy includes the Allan Gray Australia Equity Fund and institutional mandates that share the same investment strategy.

While it is trite these days to hear a company blame poor performance on weather, suppliers of agricultural chemicals do find it difficult when there is a drought, as demand drops. That has been the case in Australia, which has meant farmers have not needed anywhere near the normal quantities of agricultural chemicals. With Nufarm’s larger manufacturing and formulation base here, this has resulted in a large build-up in inventory and even more debt on Nufarm’s balance sheet. On top of this, floods and wild weather in the US have delayed planting there, further reducing demand for Nufarm’s products.

Nufarm has also experienced some integration issues with some products from the European portfolio acquisitions, as it has had trouble with the supply of one profitable product in particular. This has reduced earnings from that portfolio this year and, like a company that misses prospectus forecasts post-IPO, some serious punishment has been meted out by the market.

In addition, trade war rhetoric and tariffs have ramped up over the course of the year. Because Nufarm obtains its active ingredients from China (like many industry players) and because its customers grow things like soybeans that are exported to China, the company could stand to lose on both sides of the trade war equation.

All of this would be bad, but there is a (very sour) cherry on top of this cake. Nufarm is a supplier of glyphosate (making up approximately 10% of its gross profits), a chemical that is now being linked by some previous users to causing their cancer. The lawsuits are currently against Bayer (which bought Monsanto, the company that patented the weedkiller known best by its brandname, Roundup) and a couple of them have resulted in large damages being awarded against that company. There may be worries that Nufarm could also face lawsuits given its status as a supplier, and when the first lawsuit’s damages bill was announced, both Bayer and Nufarm’s stock prices fell sharply.

…And what could go right?

It is at these bleak times that we often see the best opportunities. Current bottom-end of range guidance sees Nufarm’s earnings before interest, tax, depreciation and amortisation (EBITDA) at $440 million and capital expenditure (capex) of around $160 million in the future, resulting in a cash flow before interest and tax of $280 million. At current prices, Nufarm’s enterprise value (its market capitalisation plus its net debt) stands at around $3.2 billion, putting the company on a little over 11 times enterprise value to free cash flow. The market is trading at much higher multiples.

Given all the headwinds Nufarm has encountered, it is hard to believe that 2019’s earnings are not low in the cycle. Paying 11 times reasonably depressed earnings looks quite attractive. On top of this, inventories are elevated, so an organic unwinding of that inventory position should reduce net debt considerably, which is what happened the last time the company recovered from a drought.

But an investment here is not without its risks

Nufarm’s debt is uncomfortably high and any missteps would require a capital raising, which the market may be fearing. While we hope that the company can do the hard work and get itself out of this situation the old fashioned way, a capital raising on its own would not destroy value, but would reduce the possible upside. There is also some risk around the acquisitions Nufarm has conducted recently. It is hard to know what normal earnings at Nufarm really look like as a result, and cash flows have historically been poor. High debt might result in greater discipline on that particular front.

And then there is glyphosate. We don’t know how that issue may unfold. Regulatory bodies around the world, including the US EPA recently, have approved glyphosate use based on scientific evidence. Even if there were a direct link between glyphosate and cancer, it is unclear what liability Nufarm would have, especially as a distributor of the active ingredient (as opposed to a manufacturer). Nufarm performs a similar service for glyphosate as pharmacists perform for approved medicinal drugs. Where these drugs are subsequently found to cause harm, it is not the pharmacist that is generally liable. If the chemical is banned, then Nufarm and other suppliers would need to supply other less-effective, often more expensive, chemicals in possibly greater quantities to meet the needs of farmers. One of those possible replacement chemicals is 2,4-D, in which Nufarm has a very strong presence through its manufacturing facilities.

While there are risks in investing in Nufarm today, we believe the company is currently priced for many of those risks eventuating and persisting. If the company can do the hard work to restore the strength of the balance sheet without raising capital and if those risks do not persist, then investors should be rewarded.

You can read the full Quarterly Commentary here.

Simon Mawhinney is the Managing Director and Chief Investment Officer at Allan Gray Australia. He holds a Bachelor of Business Science (First Class Honours) with majors in Finance and Business Strategy and a Postgraduate Diploma in Accounting (University of Cape Town). Simon qualified as a Chartered Accountant in 1998 and is a CFA Charterholder.

Dr Suhas Nayak holds a Bachelor of Science with Honours (California Institute of Technology) and a Doctor of Philosophy in Mathematics (Stanford University).