In this second post in our blog series about Allan Gray’s investment process, Analyst Justin Koonin reveals how we come up with those shares that we think will be winners.

In this second post in our blog series about Allan Gray’s investment process, Analyst Justin Koonin reveals how we come up with those shares that we think will be winners.

There are currently about 2,200 shares listed on the ASX, of which Allan Gray is invested in about 50. That’s a lot of company information to sift through, and we are often asked how we sort through the list to come up with those we think will be our nuggets of gold.

At first pass, we use a quantitative screen to limit the plausible ‘investment universe’. Allan Gray’s investment philosophy – long-term, contrarian, fundamental – filters through into our use of quantitative data.

We have written extensively about our long-term and contrarian approach, but less on how these ideas influence our fundamental analysis, and this is where this blog post will focus.

Fundamental analysis – a comprehensive health check for companies

The bedrock of fundamental analysis of shares lies in a careful examination of the many financial metrics which point to a company’s health. We screen for companies based on ratios including price-to-book, price-to-earnings, return on equity (and their enterprise-wide equivalents, which look at the impact of both debt and equity) and several others.

However, many investors use these same techniques to analyse shares. What does Allan Gray do to stand out from the crowd?

Gaining an edge in a competitive landscape

Firstly, we prioritise our long-term view in the fundamental analysis itself.

While we use financial metrics to look at recent rates of return, we also study long-term averages. It is easy to be deceived by recent rates of return for shares which deviate sharply from long-term trends, thinking that this is the ‘new normal’. Often, the best clues as to the possible state of a business a few years into the future come not from looking at its recent past, but at its long-term history.

Our charting and reporting tools present data on company profitability stretching back decades, enabling us to make detailed comparisons between the present and the past. We think returns are far more likely to return to their long-term averages. Company earnings are often cyclical and it is important to assess where in the earnings cycle a company currently sits. We ask what ‘normal earnings’ through the cycle should be.

Secondly, our analysis screens for shares which have performed poorly relative to the market over recent periods. As contrarian investors we aim to buy shares at significantly below their fair value, and for this to happen it helps if they have been forgotten by the market. Shares which are well-liked by the market tend to be overpriced and to have significantly appreciated in price prior to purchase.

One way to do this is to screen on the basis of broker ratings. We are particularly interested in shares with more ‘sell’ than ‘buy’ ratings from analysts. As counterintuitive as this may seem, we see shares which have pessimism priced-in as far less risky than those riding a wave of optimism.

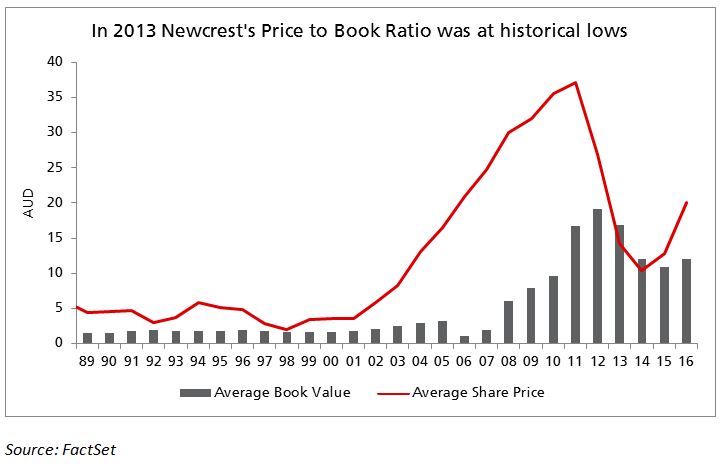

Sometimes (as in the example below) it is more the market itself, rather than the brokers, which is pessimistic about a share.

Size matters

Additionally we always look at the size (or market capitalisation) of a company. We want to invest in companies where we can take a stake that is large enough to make a meaningful contribution to our funds and therefore our clients.

Our process in action

As an example of this, in 2013 Newcrest Mining was trading at a historically low price-to-book ratio across 25 years of operation. Further research revealed a low-cost, long-life producer trading at earnings multiples well below the long-term historical average for similar companies. We bought a large position over the next couple of years and have since seen this ratio head back towards more normal levels as the share price rose, contributing to the performance investors in the Allan Gray Australia Equity Fund have recently experienced.

Of course we do not always get things right. Nor is investing as simple as making a decision based upon a single graph. Once a share is on our radar, an analyst will undertake a detailed study of the company, looking at long-term historical information, annual reports, market opinion and many other sources.

It is important to realise what quantitative screening achieves, and what it does not. Strong performance on screening tools like these does not constitute a recommendation. We use these tools to limit our attention to a smaller number of shares at a time, as a basis for further investigation.

Indeed, these quantitative methods are just the beginning of our research process. In a future blog post Suhas Nayak will go into more detail about how a share makes it from the shortlist into the fund.

Dr Justin Koonin has a Bachelor of Science with Honours and a Doctor of Philosophy in Mathematics from the University of Sydney and is a Graduate of the Australian Institute of Company Directors.