In this extract from the December 2020 Quarterly Commentary, Julian Morrison, CFA, our Head of Research Relationships and National Key Accounts, reviews the performance of the Allan Gray Australia Funds. Click here to read the full Quarterly Commentary.

In this extract from the December 2020 Quarterly Commentary, Julian Morrison, CFA, our Head of Research Relationships and National Key Accounts, reviews the performance of the Allan Gray Australia Funds. Click here to read the full Quarterly Commentary.Allan Gray Australia Equity Fund

The Australian sharemarket had a strong quarter with the ASX 300 Accumulation Index up 13.8%. The Allan Gray Australia Equity Fund (Class A) returned 23.1% during this period, outperforming its benchmark by 9.3%.

In a reversal from the prior quarter, our overweight position in the Energy sector was the largest positive contributor to relative returns. This includes stocks such as Woodside Petroleum and Oil Search. The Materials sector was also positive overall, with Alumina and Sims contributing strongly to relative performance, which more than offset underperformance from Newcrest Mining. We continue to view the abovementioned companies as sustainable businesses with strong balance sheets that offer particularly attractive value relative to the market.

Elsewhere, the Fund’s underweight position in Healthcare contributed strongly to relative performance as that sector fared poorly during the quarter. We have long held the view that some of the stocks in this sector have been priced with excessively optimistic expectations, and remain wary of the risk of overvaluation.

On the negative side, the underweight exposure to Information Technology was the largest detractor on a sector basis. However, the detraction was not particularly substantial versus the overall portfolio, which featured a high proportion of outperformers for the quarter.

We continue to see great opportunity in discounting the obvious, and investing where others are not looking. These opportunities are among longer-standing companies that have a proven track record, and a sound basis to exist, but which for some reason have appeared unappealing to most investors.

Despite the strong performance in the last quarter, the recovery to date has been relatively immaterial in the context of the preceding underperformance, and similar past experiences. We see significant unrealised value in the Fund versus the market and thus remain optimistic about future long-term prospects.

Allan Gray Australia Balanced Fund

The Allan Gray Australia Balanced Fund returned 12.8% for the December quarter, outperforming its composite benchmark by 7.5%.

The Fund has been overweight equities versus fixed income. This contributed positively to relative performance for the quarter, as did stock selection in both Australian and global stocks. As at quarter-end, the Fund had 37% in domestic equities and 37% in global equities, though about 6% of the global equity exposure is reduced through the use of exchange-traded derivatives, which allows for some protection in those periods where market indices fall.

The Fund held around 21% in fixed income securities and 5% in gold at quarter-end. The fixed income allocation has remained significantly shorter in duration than the benchmark – below two years versus seven for the benchmark. This contributed to outperformance for the December quarter, with government bond yields generally rising during the quarter. The Fund remains more defensively positioned than the benchmark in terms of both relative and absolute returns, in the event that interest rates rise further. The exposure to gold detracted slightly from relative performance for the quarter and we retain that position. As with the Equity Fund, we believe portfolio value relative to the market is significant, and we continue to manage for risk with a long-term, valuation-driven perspective.

Allan Gray Australia Stable Fund

The Allan Gray Australia Stable Fund delivered 7.2% for the December quarter, outperforming its cash rate benchmark, which delivered just above 0%.

The performance of the Stable Fund is driven by the performance of our favoured Australian share holdings and the decision on how much is invested in shares versus cash. Having added to share exposure during the weakness of the prior quarter, the Fund took advantage of the strength of the December quarter to lighten many positions. One exception to this was Newcrest Mining, to which we added on relative weakness.

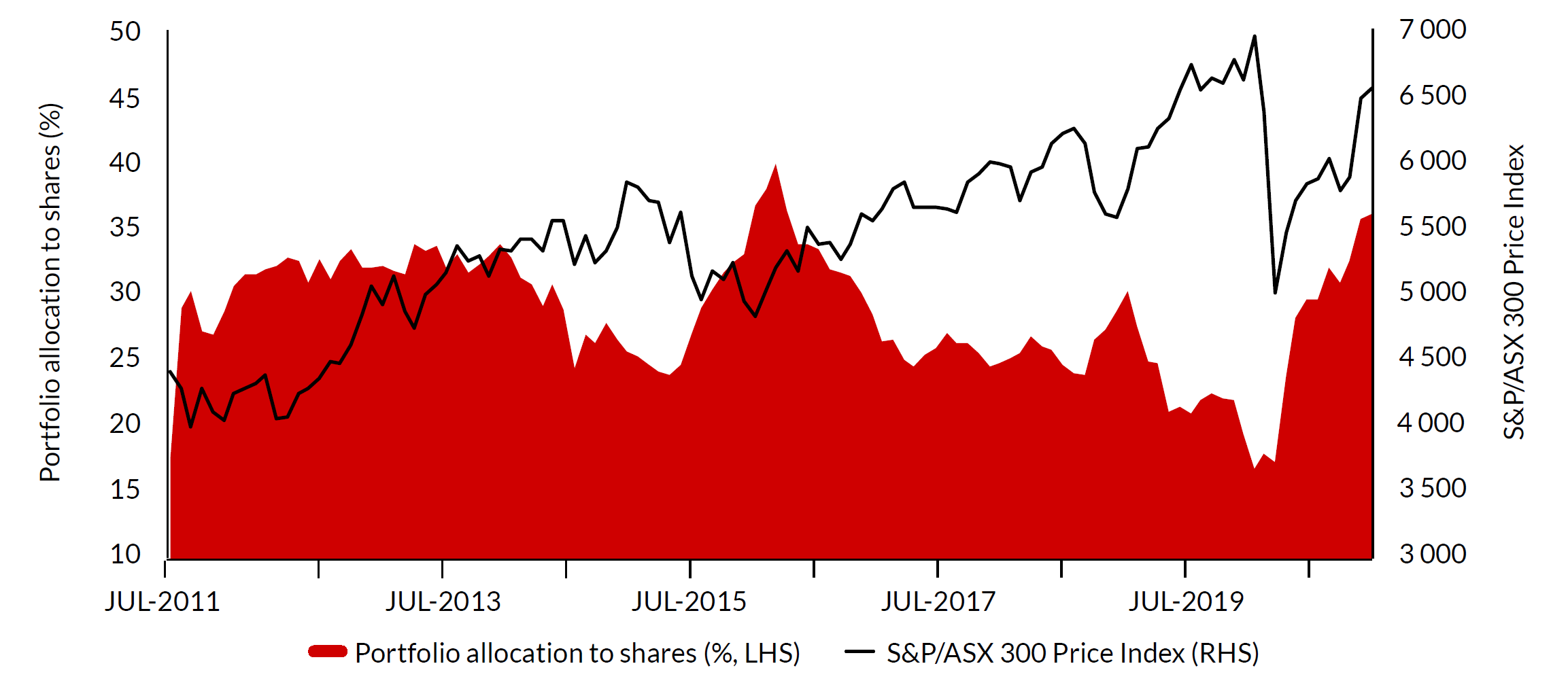

As at the end of December, the Fund had around 36% invested in shares, with the remainder in cash and money market investments. (This can be seen in the graph below, which shows our allocation between cash and equities over time.).

The overall recovery in the sharemarket during the last quarter fails to highlight the significant divergence that has built up over time between different categories of stocks. Some popular stocks and sectors are priced at levels that in our view are far too optimistic. We therefore remain focused on avoiding those areas and the risks that come with excessive valuation. Instead, the shares held in the Fund will be those we have assessed as most attractively priced, and where we believe the risk of permanent capital loss is low.

Stable Fund share weighting – share allocation rises where we see value in shares

Source: Allan Gray, Bloomberg, as at 31 December 2020.

Julian Morrison holds a Bachelor of Arts (Honours – University of Sheffield) and the Chartered Financial Analyst designation.