Quarterly Fund review – December 2021

Quarterly Fund review – December 2021

In this extract from our December 2021 Quarterly Commentary, Julian Morrison, CFA, our Investment Specialist, reviews the performance of the Allan Gray Australia Funds. Click here to read the full Quarterly Commentary.

Allan Gray Australia Equity Fund

The Australian sharemarket had a positive quarter to 31 December, with the S&P/ASX 300 Accumulation Index up 2.2%. The Allan Gray Australia Equity Fund (Class A) returned 0.9% during the same period, underperforming its S&P/ASX 300 Accumulation Index benchmark by 1.3%.

On a monthly basis, the Fund outperformed its benchmark in October, with all of the quarterly underperformance coming in November. In December the Fund recouped some of this as it moved back into strong outperformance for the last month of the year.

During the quarter, positioning in the Energy sector was the largest detractor, followed by some share-specific holdings in the Materials sector. Within those, Alumina, Woodside Petroleum and Oil Search were leading detractors. It was far from one-way traffic however, as positive contribution to relative performance came from Sims, Incitec Pivot, Newcrest Mining, South32, and Worley.

Within the Energy sector, we believe significant undervaluation remains, so we continue to hold meaningful positions here. We also added further to engineering services company, Worley, during the quarter. The shares held in Oil Search were exchanged into Santos shares in December, following the previously announced merger.

The Financials sector was mixed, with outperformance from NAB partially offsetting underperformance from Westpac. Within Financials, the banks have performed strongly over the last year and we lightened exposure a little further during the quarter. However, the reduction in exposure came from the strongly outperforming NAB and we shifted some of this into Westpac on relative weakness.

Elsewhere, strong positive contribution to relative performance came from Metcash in the Consumer Staples sector and we reduced this position meaningfully at higher prices. The absence of exposure to Information Technology and Healthcare both also aided relative performance, as those sectors underperformed.

The back and forth in performance has continued this quarter as the market oscillates on matters of valuation and overall outlook. For example, Energy and Materials were the largest detractors by sector this quarter overall, after being the strongest contributors in the prior quarter. However, in December, Materials and Energy once again contributed strongly, (as did our underweight position in Healthcare). This may well suggest that the demise of Energy, certain Materials, and other unloved shares, and the limitless rise of ‘growth’, disruptive technology, healthcare and other favourites, is no longer a foregone conclusion. And perhaps reasonable doubt has entered the minds of investors.

We are mindful that the relative fortunes of companies are often not obvious and, at extremes, the future reality can be very different to the most strongly held consensus opinions. When those differences are realised can be where share prices move most violently – in both directions.

Therefore, the focus on valuation and patience remains critical at a time when many are capitulating on that discipline. The risk of trying to ride today’s favourite shares endlessly upward is, in our opinion, much greater than seems to be appreciated. Counter to this, we have positioned the Fund where we see significant latent unrealised value and so we remain optimistic regarding future long-term prospects for outperformance.

Allan Gray Australia Balanced Fund

The Allan Gray Australia Balanced Fund returned 0.7% for the quarter, underperforming its composite benchmark by 1.2%.

The allocation to shares contributed positively to absolute performance. However, share selection in global shares detracted from relative returns and was the primary contributor to underperformance for the quarter. The allocation to Australian shares was broadly neutral in terms of relative performance.

The Fund had 69% in shares as at 31 December 2021. This is after accounting for about 8% of the global share exposure being reduced through the use of exchange-traded derivatives, which allows for some protection in those periods where market indices fall.

As at 31 December 2021, the Fund also held around 17% in fixed income securities and had a 5% exposure to gold through an exchange-traded fund. The fixed income allocation has remained significantly shorter in duration than the benchmark – at below two years versus more than seven years for the benchmark.

This means that the fixed income portion of the Fund remains more defensively positioned than the benchmark (in terms of both relative and absolute returns), in the event interest rates rise from current historically low levels. Longer-term interest rates did indeed rise during both the last quarter and the prior quarter. This positioning contributed positively to relative performance during both periods and we believe this continues to be a prudent position to hold.

As with the Equity Fund, we believe potential portfolio value relative to the market is significant and we continue to manage risk with a long-term, valuation-driven perspective.

Allan Gray Australia Stable Fund

The Allan Gray Australia Stable Fund returned 0.0% for the quarter, materially in line with the cash rate benchmark quarterly performance. The Fund outperformed in October and December, offsetting the underperformance experienced during November.

The performance of the Stable Fund is driven by the performance of our favoured Australian share holdings and the decision on how much is invested in ASX-listed securities versus cash. The broad Australian sharemarket has risen strongly for five consecutive quarters now and remains not far from all-time highs. The Fund took advantage of the recent strength to lighten some of the positions that have risen to around fair value or beyond. We have also maintained positions in some shares which have risen, but which are still significantly below fair value, and added to others on weakness.

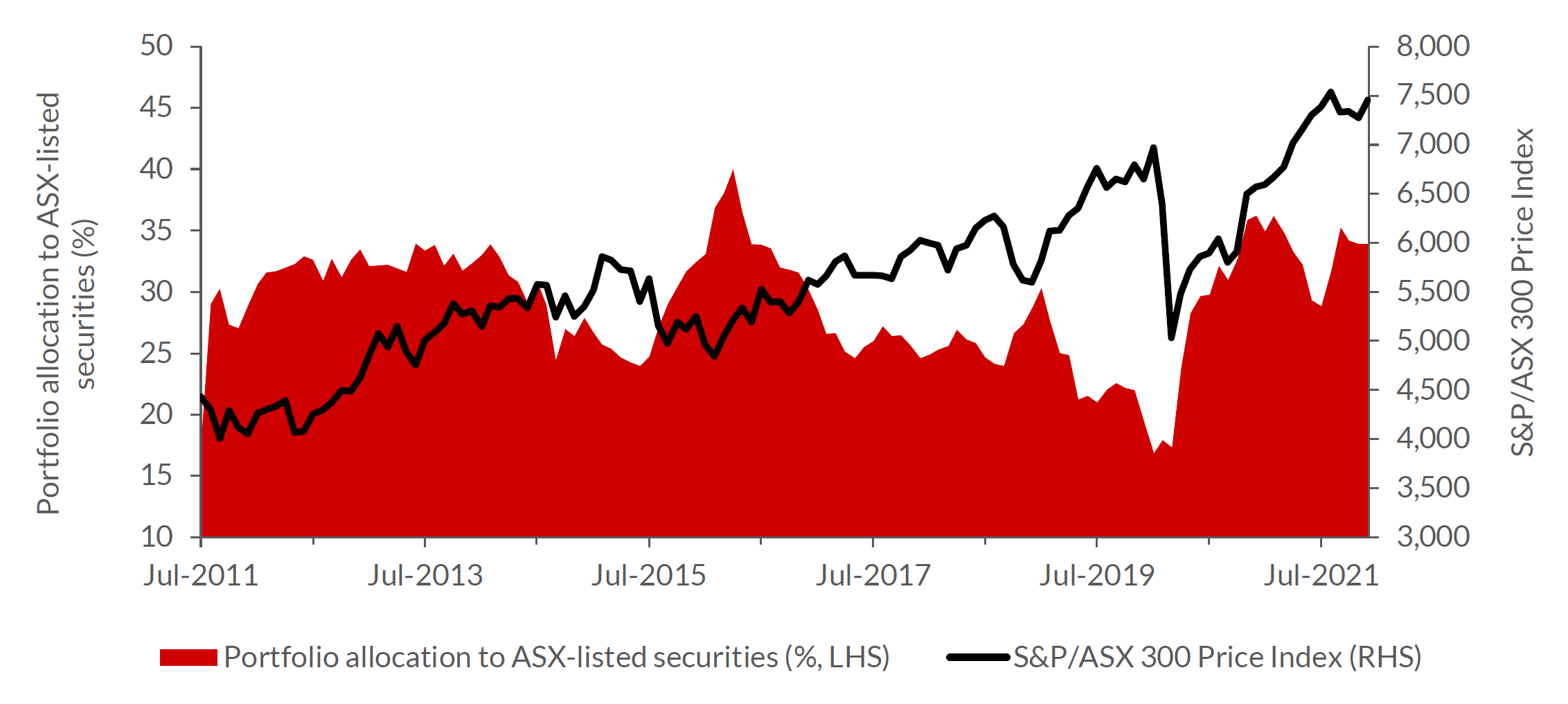

As at the end of December, the Fund had around 34% invested in ASX-listed securities, the remaining 66% is held in cash and money market investments. (This can be seen in Graph 1, which shows our allocation between cash and ASX-listed securities over time).

The extreme strength in the sharemarket during the last year fails to highlight the significant divergence that has built up over time between different categories of shares. Some popular shares and sectors are priced at levels that are, in our view, far too optimistic. We therefore remain focused on avoiding those areas and the risks that come with excessive valuation. Instead, the shares held in the Fund will be those we have assessed as most attractively priced and where risk of permanent capital loss is low.

Graph 1: Stable Fund listed security weighting – allocation rises where we see value in listed securities

Source: Allan Gray, Bloomberg, as at 31 December 2021.

Julian Morrison holds a Bachelor of Arts (Honours – University of Sheffield) and the Chartered Financial Analyst designation.