Is the sharemarket expensive? Not overwhelmingly, but there is a huge difference between sectors. Unfortunately the path to outperformance is not as easy as buying those sectors trading at the lowest valuations. In this extract from the March 2018 Quarterly Commentary Simon Mawhinney discusses why he believes we are well positioned to take advantage of these different valuations and why relative returns from here could be strong.

This quarter has not been our finest, with the Australia Equity Fund strategy (the portfolio) underperforming the market. There is reason to be optimistic about the portfolio’s future earnings and relative valuation, however.

When it comes to assessing valuation, market commentators spend a lot of time opining on the ratio of a company’s share price to its recent past and near-term future earnings (its historical and forward PE ratio), and on how that multiple compares to the past. Too often though, these ratios focus on the numerator: price. This is unsurprising, as the price you pay for a company really matters.

But so do the earnings. A company’s value is the present value of the future cash flows which an investor will receive from that company. For an investor with an infinite investment horizon, this is mostly in the form of dividends. It is future earnings which drive the level of these future dividends and an assessment of where current earnings are in their cycle, and therefore how sustainable they are, is important.

The valuation trade-off

Investors are usually faced with some form of trade-off: buying depressed earnings at somewhat inflated multiples, or buying inflated earnings at depressed multiples. The other two options are either rare (being fortunate enough to buy low or depressed earnings at low multiples) or a sure path to financial ruin (buying inflated earnings at inflated multiples). It may seem counter-intuitive, but some of the best investments in the portfolio over the last 10 years have been the result of buying depressed earnings at very high multiples. Relative to normalised earnings, these companies turned out to be very attractively priced when we first bought them.

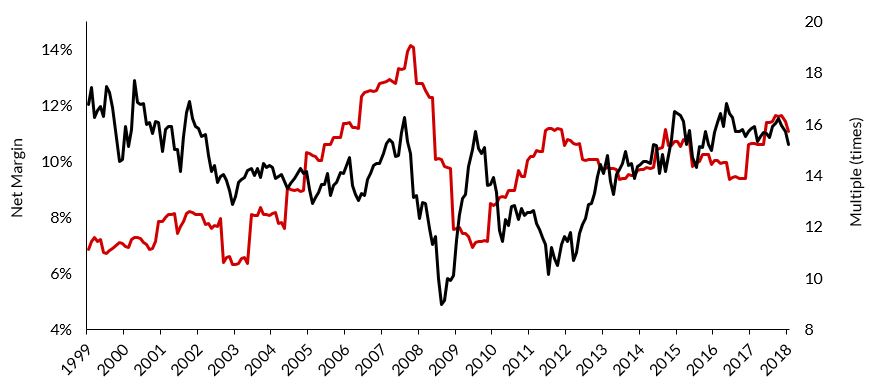

Graph 1: S&P/ASX 300 Index PE multiples and margins

Source: Factset, 31 March 2018

Graph 1 reflects the one-year forward PE ratio of the S&P/ASX 300 Index since 2000 (black line). The current level of close to 16 times earnings is similar to levels that have prevailed since 2015, but are above historical averages. Profitability has also increased in recent years and is up significantly on its post-financial-crisis lows in 2009. This is evident from the red line, which graphs the overall market’s net margin (a measure of profitability). It is hard to argue that company profitability today is low, but equally hard to argue that multiples of these profits are particularly high.

Is the sharemarket expensive?

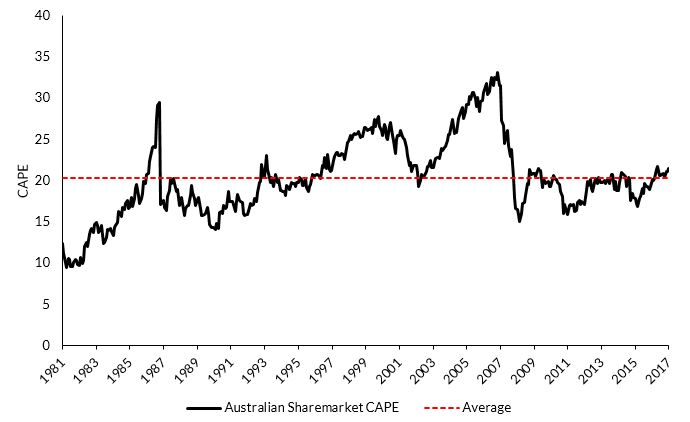

The Cyclically Adjusted Price Earnings ratio (CAPE) is another way to assess valuations. The CAPE compares the current market level (price) to the average of the past 10 years’ earnings, adjusted for inflation.

As Graph 2 shows, on this measure, the Australian sharemarket trades at a multiple of 21.4 times versus its own average of 20.3 times (since 1981). Our sharemarket isn’t eye-wateringly expensive relative to its history and appears to be much cheaper than the S&P 500 Index which trades on a CAPE of 31 times, over 30% higher than its average of 23 times.

Graph 2: Cyclically Adjusted Price Earnings ratio (CAPE) since 1981

Source: Barclays, Shiller. Data is presented to 31 December 2017.

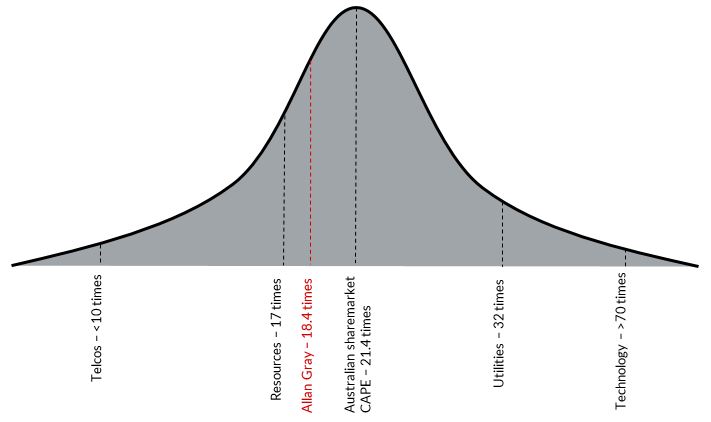

But the less a portfolio looks like the broader sharemarket, the less helpful this CAPE analysis is. Various sub-sectors of the market trade at multiples of historical average earnings which are very different from the 21.4 times average referenced above. This is illustrated in Graph 3 (not to scale) with the two sector extremes being the technology sector on over 70 times cyclically adjusted earnings and the telecommunications sector on less than 10 times.

Graph 3: CAPE analysis of market sectors

Source: Factset. Chart not to scale. 31 March 2018

If only the path to riches was as easy as buying the companies/sectors trading at the lowest multiples of historical earnings. Unfortunately the technology sector is not necessarily seven times as expensive as the telecommunications sector. Technology earnings have almost doubled over the past 10 years and are expected to grow further next year, resulting in the sector trading at about 27 times next year’s consensus earnings. Were that growth to continue, the sector could currently be extraordinarily cheap. Equally, the telecommunication sector’s historical earnings cannot be sustained. Most of this sector’s earnings come from Telstra Limited whose earnings are in transition following the roll out of Australia’s National Broadband Network. If earnings fall significantly from here, 10 times earnings might be expensive.

Solely focussing on the CAPE has other shortcomings too. Companies and sectors may have undergone structural changes which make the future very different to the past and when it comes to investing, it is future earnings that matter! A sector or company may have invested heavily in productive assets over the past 10 years resulting in reasonable expectations of higher future earnings.

Valuing the portfolio against the market

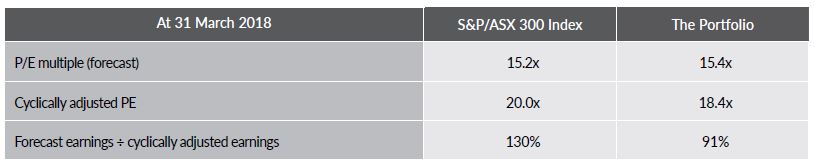

In trying to assess the portfolio’s relative valuation, we have tried to identify, company by company, where we are in its earnings cycle and how much one pays for those earnings. Table 1 reflects some of our findings, which are expressed at the overall portfolio level.

Table 1: S&P/ASX 300 Index valuation versus the portfolio

Note: A company’s enterprise value is its market capitalisation plus its net debt.

Source: CapitalIQ, Factset, Allan Gray, 31 March 2018

The portfolio and broader sharemarket trade at a similar multiple to next year’s consensus earnings. However, there are reasons to believe that the portfolio’s earnings are significantly more depressed than the sharemarket’s.

The portfolio’s earnings are well down on historical levels with next year’s forecast earnings 9% below cyclically adjusted levels. This compares to the sharemarket whose earnings are forecast to be 30% above their cyclically adjusted average. For a similar price, at face value, investors are buying an earnings stream which is nearly 40% more depressed than the sharemarket. The portfolio’s CAPE is 18.4 times and modestly below the market’s at 20 times.

But do these depressed earnings mean the portfolio is cheap relative to the broader sharemarket? Not necessarily. You could argue that the portfolio’s earnings are likely to grow more slowly than the sharemarket and should command a lower multiple. Or worse, that they’re structurally impaired and not cyclically depressed, with future earnings likely to be even lower than current earnings. You could also conclude that an analysis of historical earnings is irrelevant unless assessed together with the amount a company has invested in its future earnings, both organically and via acquisition. On each of these plausible pushbacks, the portfolio fares reasonably well relative to the broader market.

Consensus estimates put the portfolio’s earnings growth at 12.9% in 2019, well above the sharemarket’s earnings growth and not reflective of a portfolio in terminal decline (of course, consensus could be wrong). The portfolio has also invested very heavily in the future. This is best evidenced by the number of shares each company has on issue – an increasing amount is generally accompanied by some form of investment or debt reduction. The portfolio’s weighted average shares on issue is 18% above the average of the past 10 years, a sign of significant investment over recent years. Expectations of future earnings growth in excess of the market is therefore not unreasonable, even if the proceeds from this share issuance were simply used to pay down debt.

Despite the difficulty in presenting a fail-proof measure of valuation, it appears that we pay a market multiple for an earnings stream which, in all likelihood, is significantly more depressed than the overall sharemarket. If we’re right, opportunities like this are rare and relative returns from here could be strong. If we are wrong, the downside doesn’t appear to be large. Just the kind of pay-off profile we like.

You can read the full Quarterly Commentary here.

Simon Mawhinney holds a Bachelor of Business Science (First Class Honours) with majors in Finance and Business Strategy and a Postgraduate Diploma in Accounting (University of Cape Town). Simon qualified as a Chartered Accountant in 1998 and is a CFA Charterholder.

Can you explain what caused the increase of distribution of 12cents per unit for the Australian equity fund July 2018 compared to the distribution of 5.8cents per unit last year July 2017. Regards Caleb.

Hi Caleb, this is largely capital gains related. A member of our Client Services team will contact you directly.