This is an extract from our June 2022 Quarterly Commentary and you can read the full Quarterly Commentary here.

Simon Mawhinney, CFA, Managing Director and Chief Investment Officer

This year has seen a recovery in the performance of Value managers with the narrative now moving from “Is Value investing dead?” to “Is it time to buy Growth companies?”. The Growth versus Value debate seems impossible to win.

For us, the categorisation between Growth and Value is, in isolation, arbitrary. Instead, we focus on the fundamental drivers of value for all companies, specifically the future earnings (and cashflows) a particular investment is likely to generate.

But before getting to these fundamentals, here are some high level observations on where we are in the Growth and Value cycle. MSCI, a leading index provider, segments the universe of shares into Value indices and Growth indices according to their style characteristics. Certain variables are used to determine the Value universe (e.g. book value to price ratio, 12-month forward earnings to price ratio, and dividend yield) and other variables are used to determine the Growth universe (e.g. earnings per share growth rate and long-term historical sales per share growth trend). Depending on how they score, some shares are partially allocated to both indices and each index is reviewed twice a year.

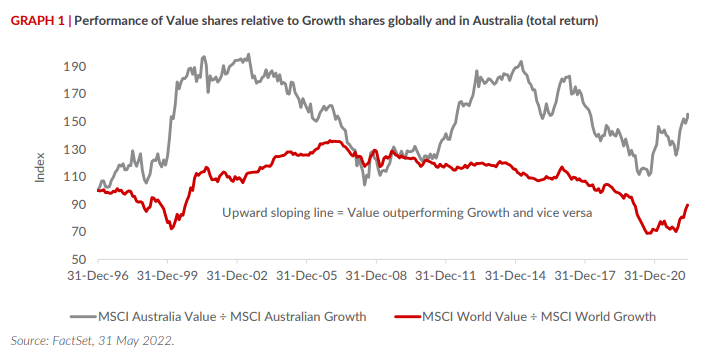

Graph 1 shows the performance of the MSCI All Country World Index (ACWI) Value Index relative to the MSCI ACWI Growth Index since 1996 (red line) and the same for the equivalent Australia-only indices (grey line). When a line is sloping upwards, Value is outperforming Growth and vice versa.

We will focus on the global ACWI line (red) first. As readers might expect, Value significantly underperformed Growth during the technology bubble of the late 1990s. As the bubble burst, Value shone until the onset of the Global Financial Crisis. Despite brief periods of reprieve, the next 13 years were brutal for Value managers and it is only recently that they’ve begun licking their wounds and sticking their heads above the parapet. If price is anything to go by, Value still appears to be very depressed and barely back at pre-COVID-19 relative levels.

What’s the story in Australia?

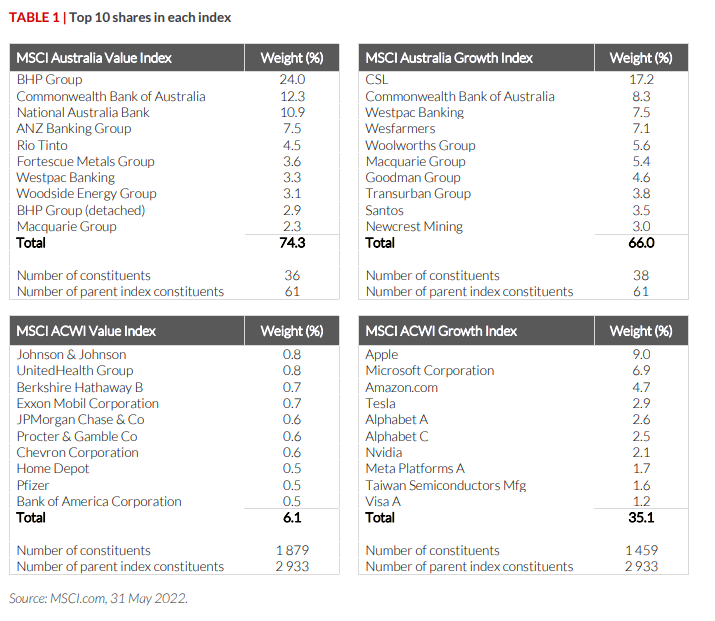

The Australian experience (grey line) is wildly different, with Value far less depressed (and arguably inflated if the starting point in 1996 is anything to go by). Why is this and can these categorisations be relied upon? The answer lies in the composition of each index. Table 1 shows the top 10 constituents and their weights for each of the four indices that are represented in Graph 1.

With only 61 constituents in the parent MSCI Australia Index, it is no surprise that the top 10 constituents comprise a large proportion of both the Value (74.3%) and Growth (66.0%) subindices. But it is the extreme skew to iron ore miners and banks that makes the MSCI Australia Value Index less representative than the MSCI ACWI Value Index. Three iron ore miners and

our big four retail banks make up close to 70% of the Australia parent index and 90% of the top 10 constituents. This level of concentration is not the case in the MSCI ACWI indices. With a backdrop of inflated iron ore prices and a 30-year credit boom for our banks, it’s no wonder Value in Australia has fared so well.

Two other factors make comparisons between the performance of the Australia sub-indices difficult:

- There is a large degree of overlap between the two subindices. Commonwealth Bank of Australia, Westpac and Macquarie Group are large constituents of both the Value

and the Growth index (this degree of overlap does not exist in the ACWI). - Companies with nearly identical fundamental value drivers are separated into different sub-indices. Woodside Energy Group and Santos (both oil and gas producers) are examples

of this.

These anomalies also exist in the ACWI sub-indices, but given the significantly reduced weights of the constituents, it doesn’t impact comparability in the same way. Not only is the ACWI far more diverse, but Australia’s 2% weight in this index is low enough not to create similar distortions.

In short, unlike the ACWI, the relative returns of the MSCI Australia Value Index and the MSCI Australia Growth Index are of little relevance and at best illustrate how a small cross section of iron ore miners and banks have performed. Even then, it is a little noisy! But globally, as judged by price performance alone, Value still appears to be very depressed.

How is this relevant?

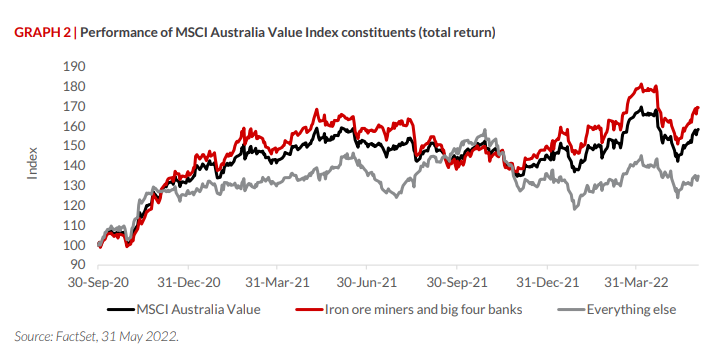

Despite the noise around the composition of the Australian subindices, there are two important observations we make with regard to our portfolio. Firstly, the Allan Gray Australia Equity portfolio has no iron ore exposure (a large detractor from our recent performance) and is also significantly underweight the banks (another detractor). We feel better value is available elsewhere and, as a result, we own much of the remaining constituents, which have lagged the MSCI Australia Value Index by a considerable amount. This is illustrated in Graph 2.

Despite share prices of the ‘everything else’ constituents lagging the Australia parent index, the underlying drivers of their earnings have been every bit as strong as the iron ore miners and banks. Look no further than the recent strength in energy prices, base metal prices, fertiliser prices or scrap metal prices to name a few.

The second observation relates to the rise of passive investment and the impact it has on share prices. A growing number of exchange-traded funds (ETFs) have been established to replicate and track indices such as those MSCI compiles (including subindices like the MSCI ACWI Value Index). The ETFs do this by investing in the underlying constituents of the relevant index. A company’s inclusion in an index and its periodic reweighting has a meaningful bearing on the buying appetite for a constituent company (and vice versa). The fact that the MSCI Australia Index only has 61 constituents (a small fraction of our Equity portfolio’s investable universe) and that these are heavily weighted towards iron ore miners, banks and a few healthcare companies, has likely caused extreme price dislocations as the weight of money flowing into index-tracking ETFs influences prices.

Our portfolio has little exposure to these index heavyweights and has therefore not benefited from the wave of money that these ETFs have attracted. The lack of depth in Australia’s MSCI constituents has meant that some companies in Australia have fared far worse (in price terms) than comparative companies overseas that are well represented in the MSCI indices.

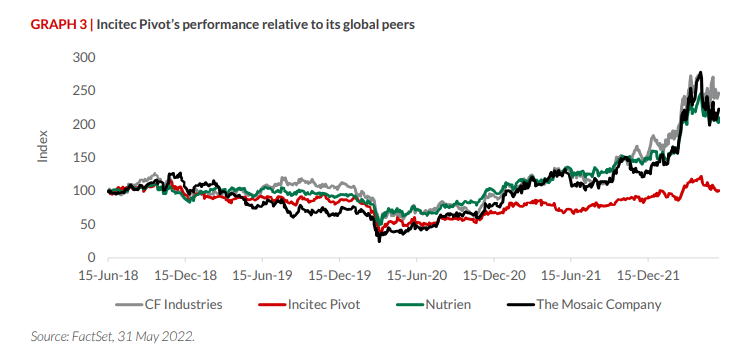

One example, that our Equity portfolio holds, is Incitec Pivot Limited, a fertiliser and ammonia producer. It is not in the MSCI Australia Index (and therefore not in the ACWI or its subindices), whereas its global peers The Mosaic Company, CF Industries, Nutrien and Yara are represented in the ACWI. Graph 3 shows Incitec’s performance relative to its peers.

Admittedly, Incitec has had its fair share of operational hiccups over the past five years, but it feels like this has been disproportionately reflected in its relative share price performance. There are many other examples too, across different sectors, which suggest share price underperformance might be a result of index underrepresentation (rather than company-specific operational outcomes). For example, our Equity portfolio also holds:

- Sims Limited, which has significantly underperformed global steel companies

- Woodside Energy Group Limited, which has underperformed global energy companies, and

- QBE Insurance Group Limited, which has underperformed global insurers.

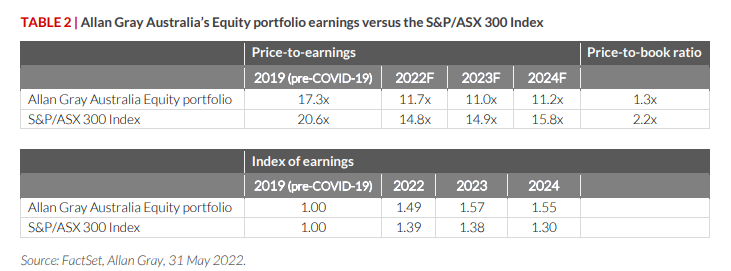

This is not all bad news. In fact, in some ways it’s very good news. We have been able to accumulate portfolio holdings at lower prices relative to the overall market. Table 2 shows the multiple of consensus earnings forecasts that our Equity portfolio trades for, versus the broader sharemarket. It shows our portfolio of companies growing faster than the broader sharemarket, but trading at a significant discount to the market (11 times earnings versus the market’s near 16 times).

The headwinds we’ve written about above have had at worst, a medium-term impact on our performance. Pendulums swing both ways and this should ultimately benefit the portfolio. It’s not clear what the catalyst for a correction will be, however, or when this will happen. Perhaps it will be passive funds experiencing outflows, which would disproportionately benefit our portfolio. Or some other unforeseeable outcome. We don’t look for catalysts when investing, we look for value, as catalysts are extremely difficult to predict.

What we do know is that the status quo doesn’t appear to be sustainable. In the meantime, the Equity portfolio offers defensive qualities today, potential significant outperformance if and when the pendulum swings the other way and, until then, its dividend stream pays us to hold them. What’s not to like?