By on 10 May 2019

By on 10 May 2019There’s no place like home

Unless of course it’s difficult to find one. This begs the question as it applies to new investment funds offered up by the funds management industry – what drives a new fund launch? You would hope and think that most managed funds are created to meet client needs, but the reality is that this is rarely the main driver.

Unless of course it’s difficult to find one. This begs the question as it applies to new investment funds offered up by the funds management industry – what drives a new fund launch? You would hope and think that most managed funds are created to meet client needs, but the reality is that this is rarely the main driver.

To ensure a fund’s success in market, at least in a time frame palatable for most managers, it must be commercially viable in terms of getting fund flows from investors and will also need to ‘fit in’. Funds must ideally be able to be categorised into peer groups of funds with similar investment strategies or asset allocations.

The advantage of this is that funds can be measured and compared, which allows funds to be rated by research houses. Advice companies and dealer groups can then use these measurements to develop their recommended lists and, over time, benchmark the funds and rate their performance over the long term.

Ratings and market acceptance are critical for funds to be considered for inclusion on platforms, approved product lists and model portfolios. As a result, most fund managers will launch funds that ideally fit into existing peer groups. To choose a different path, a manager would typically need an extraordinary commitment from a client group to warrant proceeding. This commitment would provide the scale necessary to give comfort to the manager.

What’s good for the goose isn’t always good for the gander

One problem with this aspect of the industry is that many funds in a peer group can look the same, bringing less diversification for investors. Being different is often great for investors, but sometimes not so great for management teams!

When investment managers create funds to fit into a peer group or to maximise fund flow, rather than to meet client needs, investors may not get the funds they require. Although some fund managers are category unaware, our industry is simply not set up to accommodate products that don’t fit in neatly, even if this is what clients need.

We give people what they need, not what they want

We have always maintained this mantra at Allan Gray. It’s an idea that ensures we only launch products or strategies that are in the interest of investors. We do not launch products based on themes, fads or trends in order to grow our assets at the expense of long-term return outcomes of clients.

Let’s look at the simple investment objective of many investors: to beat cash.

This should be a given for just about any strategy that invests in assets deemed riskier than cash. But funds that explicitly aim to beat cash are often more complex than they need to be and use ‘alternative’ strategies such as derivatives, which can introduce additional risk. If these strategies work and the fund delivers on its cash-beating objective, the investor gets what they want. But if these strategies increase risk, the investor doesn’t get what they need. One might ask if the complexity of the products justifies their consideration. Perhaps a topic for another day.

Beating cash doesn’t need to be complicated. A simple structure of starting with a default position of cash and then building some exposure to shares via select companies can achieve the desired result, assuming you invest in the right shares.

It’s easier said than done

All investors strive to ‘Buy low and sell high’, but in practice this is extremely hard to do. The behavioural challenges investors face in doing this consistently are significant. In fact, most investors do the opposite, buying at the top of the market during periods of euphoria when it feels safe to invest and selling at the bottom of the market when attitudes are subdued.

To achieve better returns you need to do the opposite – you need to invest counter-cyclically. Investing in expensive companies hoping they become more expensive has always seemed like madness to us. Investing in companies and markets when they are undervalued should lower your risk of permanent loss because there is arguably less room to fall as you have invested with a margin of safety to fair value.

Following on from such thinking it should be logical that there is better value in these shares and accordingly they have greater capacity to rise in the future. Most importantly though, you increased the chance of protecting yourself from large losses. This strategy does of course assume that you have done your research. If successful, then perhaps you can beat cash returns but with much less volatility than the sharemarket.

In 2011 we launched the Stable Fund with this thinking in mind. We keep it simple by aiming to beat the RBA cash rate over the medium term, by investing in cash and term deposits and blending this with a portfolio of select contrarian shares. This ensures we remain true to our long-term, contrarian approach.

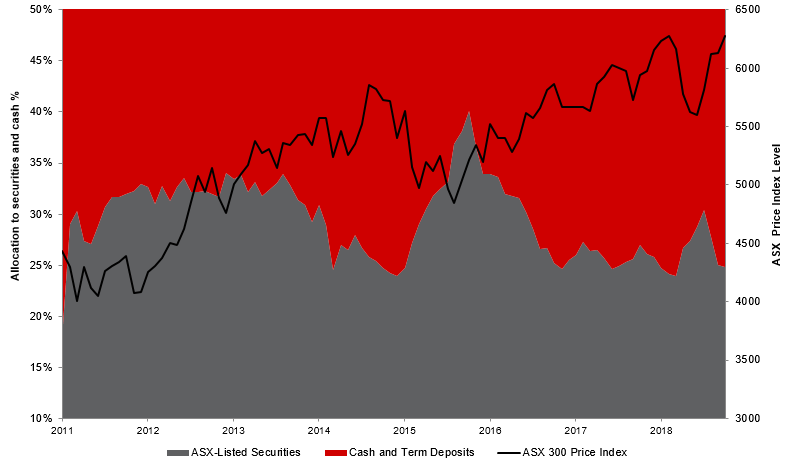

At Allan Gray we are contrarian investors, and we naturally invest counter-cyclically. We only aim to buy shares in the Fund when they represent good value and we reduce the equity exposure when the market rises. You can see in the chart that the Fund’s equity exposure has generally increased as the market falls and decreased as the market rises. You can learn more about the Fund here.

Fund portfolio weightings – share exposure increases as market falls and vice versa

Source: Allan Gray Australia as at 30 April 2019

When we launched the Stable Fund it was not readily accepted by the industry and, arguably, it still isn’t. It did not, and still does not, fit in to a nice neat category that allows for easy comparison. Ironically, its simplicity left it homeless, making it difficult to gain acceptance by the broader market.

What to do?

As the Fund has no peers, it can be hard to determine exactly how it should be used.

We have never prescribed how the Fund should be used, rather we have simply educated clients and advisers on what we are trying to achieve. In our conversations with investors they appear to have used the Fund in one of three ways:

- To control their exposure to equities in a counter-cyclical way

- Where they are concerned about broader markets and are looking for a simple and conservative option

- Where they are looking for an alternative to cash and are happy to tie up their capital for two or three years.

You can learn more about the fund here, or speak to our Client Services team for further information.

Chris Inifer holds a Bachelor of Business Economics and Finance (RMIT University) and a Postgraduate Diploma (with Distinction) in Financial Planning.

Equity Trustees Limited ABN 46 004 031 298, AFSL No. 240975 is the issuer of units in the Allan Gray Australia Balanced Fund ARSN 615 145 974, Allan Gray Australia Equity Fund ARSN 117 746 666 and Allan Gray Australia Stable Fund, ARSN 149 681 774 (Allan Gray Funds) and units in the Orbis Global Equity Fund (Australia registered) ARSN 147 222 535, Orbis Global Equity LE Fund (Australia registered) ARSN 613 753 030 and Orbis Global Balanced Fund (Australia registered) ARSN 615 545 170 (Orbis Funds). Allan Gray Australia Pty Limited ABN 48 112 316 168, AFSL No. 298487 is the investment manager of the Allan Gray Funds.

Past performance is not a reliable indicator of future performance. There are risks involved with investing and the value of your investments may fall as well as rise. This represents Allan Gray Australia Pty Limited and Orbis Investment Advisory Pty Limited’s view at a point in time and may provide reasoning or rationale on why we bought or sold a particular security for the Allan Gray or Orbis Funds or our clients. We may take the opposite view/position from that stated, as our view may change. If this article is authored by Orbis, it does not prohibit the Orbis Funds from dealing in the securities before or after this article is published. This article constitutes general advice or information only and not personal financial product, tax, legal, or investment advice. It does not take into account the specific investment objectives, financial situation or individual needs of any particular person and may not be appropriate for you. We have tried to ensure that the information here is accurate in all material respects, but cannot guarantee that it is.

You should consider the relevant funds’ Product Disclosure Statement (PDS) or Information Memorandum (IM), as applicable, before acquiring, holding or disposing units in the Allan Gray or Orbis Funds. The PDS or IM can be obtained from www.orbis.com.au and www.allangray.com.au. Target Market Determinations (TMDs) for the Allan Gray products can be found at allangray.com.au/PDS-TMD-documents, while TMDs for the Orbis Funds can be found at www.orbis.com.au on the 'Forms' page under 'How to Invest'. Each TMD sets out who an investment in the relevant Allan Gray or Orbis Funds might be appropriate for and the circumstances that trigger a review of the TMD.

Managed investment schemes are generally medium to long-term investments. They are traded at prevailing prices and the value of units may go down as well as up. There are risks with investing the Fund and there is no guarantee of repayment of capital or return on your investment. Subject to relevant disclosure documents, managed investments can engage in borrowing and securities lending. A schedule of fees and charges is available in the PDS.