As well as picking the right shares, another challenge faced by investors is deciding how much, or how little, of their savings to expose to the sharemarket. The Allan Gray Australia Stable Fund aims to help investors put their money to work at the most opportune time and take the risk off the table again when the Fund has made a profit. As the Fund celebrates its tenth anniversary this year, we revisit how the Fund is managed and how it could suit investors looking for a lower risk exposure to shares when combined with cash and the potential for better returns than cash over the long term.

As well as picking the right shares, another challenge faced by investors is deciding how much, or how little, of their savings to expose to the sharemarket. The Allan Gray Australia Stable Fund aims to help investors put their money to work at the most opportune time and take the risk off the table again when the Fund has made a profit. As the Fund celebrates its tenth anniversary this year, we revisit how the Fund is managed and how it could suit investors looking for a lower risk exposure to shares when combined with cash and the potential for better returns than cash over the long term.

The Allan Gray Australia Stable Fund simply combines a cash and money market allocation with our well-established, contrarian equity investment approach.

“When we created the Fund we wanted to create a product that was simple and that the investing public could relate to,” explains our Head of Research Relationships and National Key Accounts, Julian Morrison.

“We started with a clean sheet of paper with 100% of the portfolio in cash and cash equivalents, such as term deposits and short-term Government bonds with less than 12 months to maturity.

“Then we use our contrarian investment research to uncover pockets of value in the sharemarket. We take that cash investment and we invest some of it into those shares.”

The cash and equivalents portion of the portfolio is held primarily in term deposits with the big four banks. Morrison explains that with the cash investment, safety is the key focus and we don’t try to outperform money market managers. Where we do look to gain an edge is in the portfolio’s equity exposure, which can range from anywhere between zero and 50% of the Fund’s assets, depending on the value we see in the shares we want to buy. We will only likely approach the maximum 50% in shares when the wider market has fallen heavily, resulting in a broad and attractive opportunity set. Conversely, share exposure will only approach zero when all shares are fully valued.

In reality, both scenarios are incredibly rare and should be short-lived. Over its life, the equity composition in the Allan Gray Australia Stable Fund has ranged from the mid-teens to 40% of the Fund and averages around 30%. Share exposure currently sits around 35% of the Fund’s assets as at the end of January 2021.

The point of having cash in the portfolio is so there is always ammunition to put money to work in the market when prices periodically fall and shares become cheaper. It also helps limit downside risk. Morrison says the strategy is aimed at more conservative investors who are averse to the volatility that investing fully in the sharemarket brings, by limiting its market exposure to 50% of its assets. The Fund also helps investors with its contrarian investment strategy, by investing in shares when they have fallen and there is better value in the market. This strategy can reduce risk, while increasing potential returns as share prices rise.

The cash allocation smooths the journey, shielding investors somewhat from large market falls, but this also means that the portfolio will generally lag fast-rising markets. If you are looking for a lower-volatility Fund, the Stable Fund typically has lower volatility than other funds offering equity exposure because it is invested predominantly in cash.

Flexibility

The Fund’s current weighting to shares reflects how we are finding some great contrarian opportunities in the market. The portfolio remains heavily skewed towards cyclically-exposed companies, whose earnings are depressed and that the Fund can buy at low multiples of those depressed earnings.

“The Fund’s significant underweight to information technology and healthcare companies [the Fund has a zero weighting] is in contrast to the Fund’s significant overweight to energy and materials” explains Morrison. “The lack of exposure to the high-growth technology sector and the stable earnings streams from the healthcare and consumer staples sectors may seem extreme. But so are the prices one pays for companies in those sectors today.

“We think the opportunity to buy great value in cyclically-exposed companies is extraordinary now. The Fund is patiently holding positions that we believe offer the potential for long-term returns.”

Given that assessment of the market, it’s hardly surprising that Alumina, Woodside and Newcrest are amongst the largest holdings in the Fund at the moment.

The names above differ substantially from the 10 largest stocks in the S&P/ASX 300 Index, which is consistent with our contrarian approach.

What Allan Gray’s active approach brings to the table is the ability to pick shares that many investors discard or overlook, giving you an effective way to diversify and complement the other funds in your portfolio.

A contrarian approach

The investment philosophy is the same as we use for our flagship Equity Fund portfolio. It is based on buying shares at deep discounts to their historical value. This means we are often buying names for the portfolio that other investors are avoiding, or those that have underperformed, albeit with the discipline to ensure that the risk to the downside is limited as far as possible.

Sentiment is an important measure for signalling potential opportunities. When the broking community moves against a certain stock and puts a sell rating on it, our analysts go to work to test the community’s view. Where we disagree, there can be opportunity to pick up shares at a discount. What’s more, because the shares are out of favour, there is less competition for buying them and the team can usually get a much better price at execution than shares that are popular and rising in value.

Low volatility

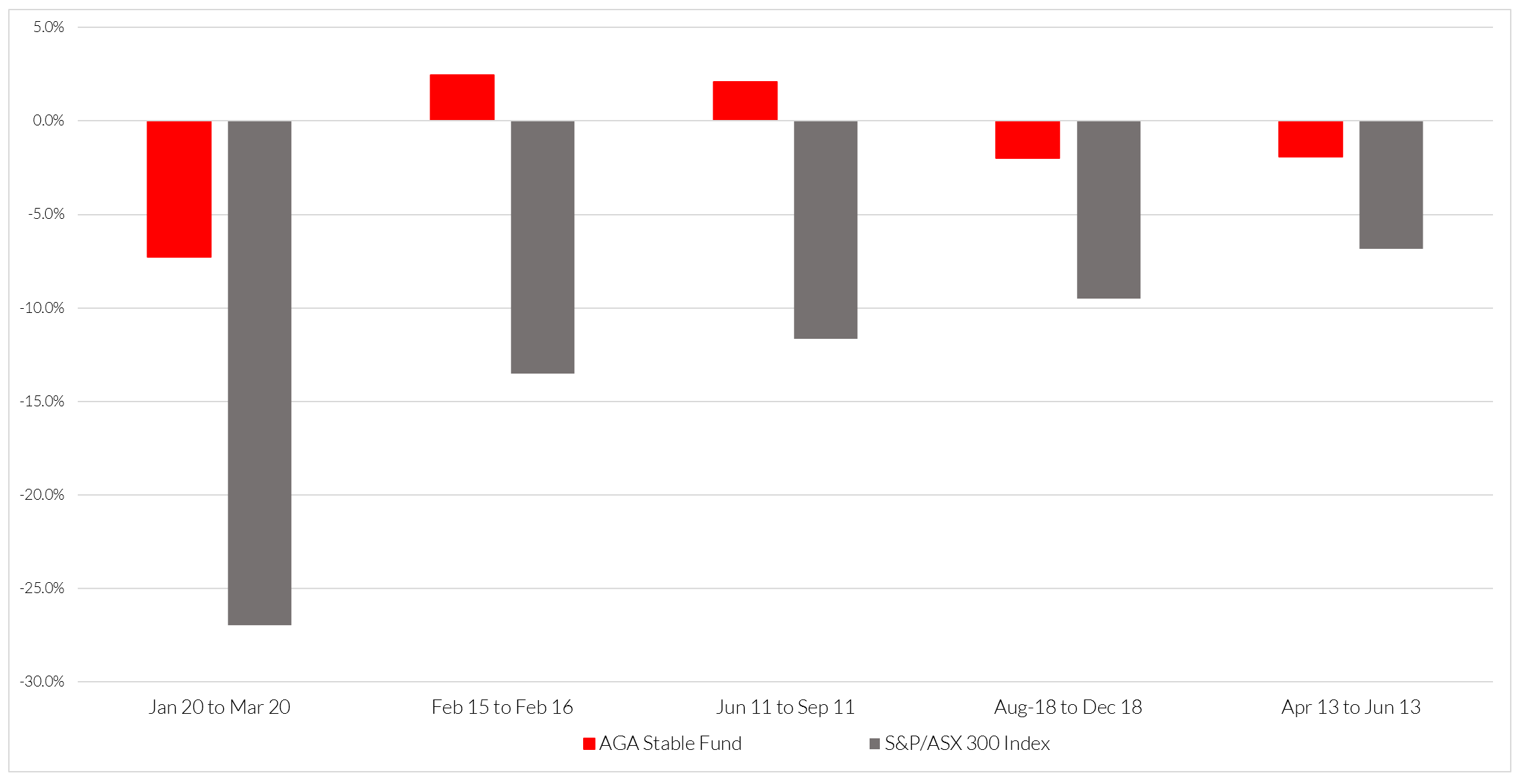

The investment experience for unit holders has been that the Fund has been a lot less volatile than the sharemarket and as at 31 January 2021 has outperformed its Reserve Bank of Australia cash rate benchmark by 4% per annum since launch in July 2011. During that time, the largest drawdown for the broad sharemarket was around -27%, while the largest drawdown for the Allan Gray Australia Stable Fund was just -7.3% over the same period.

The chart below shows the five worst drawdowns for the sharemarket since the Fund’s launch, along with the performance of the Stable Fund during those drawdowns. Over these five periods, the market’s average drawdown was -13.7%, while the Fund’s average was just -1.3%. During two of the five periods, the Stable Fund actually experienced positive returns while the market fell.

AGA Stable Fund performance during the five worst drawdowns in the sharemarket

Source: Allan Gray, drawdown and performance are based on monthly return data, Stable Fund returns include income, assume reinvestment of distributions and exclude spreads payable on those transactions

“We don’t have express volatility targets,” says Morrison. “The Fund’s main aim is to achieve inflation-adjusted returns with a very strong focus on capital preservation. We aim to do that in a way that is not overly volatile.”

In its aim to achieve a cash-plus return the Stable Fund is somewhat comparable to absolute return funds on the market. But while many of those strategies employ techniques such as long-short, options trading and use derivatives, the Stable Fund comes without any of that complexity.

“The feedback we’ve had from advisers is that they are a little concerned about lower returns from cash in future, so are willing to take some exposure to risk assets such as equities. But they are prepared to give up some upside in return for a more stable approach to meeting their inflation-beating objectives,” explains Morrison. “But they also want to know what their exposures are, and to know what the likely outcomes from different scenarios are. The Stable Fund provides this with its simplicity. It does not use gearing and does not invest in derivative instruments. You don’t necessarily get that from the more opaque structure that comes with more complicated funds.”

Click here to learn more about the Stable Fund.

Julian Morrison holds a Bachelor of Arts (Honours – University of Sheffield) and the Chartered Financial Analyst designation.