“In fiction: we find the predictable boring. In real life: we find the unpredictable terrifying.” Mokokoma Mokhonoana

“In fiction: we find the predictable boring. In real life: we find the unpredictable terrifying.” Mokokoma Mokhonoana

Our quest for predictable outcomes in our everyday lives has implications for how we invest. It is easier to invest in companies with certain or relatively predictable outcomes. Not only is it easier to sleep at night, it is also a lot easier to justify one’s investment decisions. This can create significant price distortions. The market tends to inflate the prices of assets whose outcomes are perceived as relatively predictable, while assets that are perceived to have more uncertain (or volatile) outcomes are often priced at a discount.

Stable earnings inflate a share price

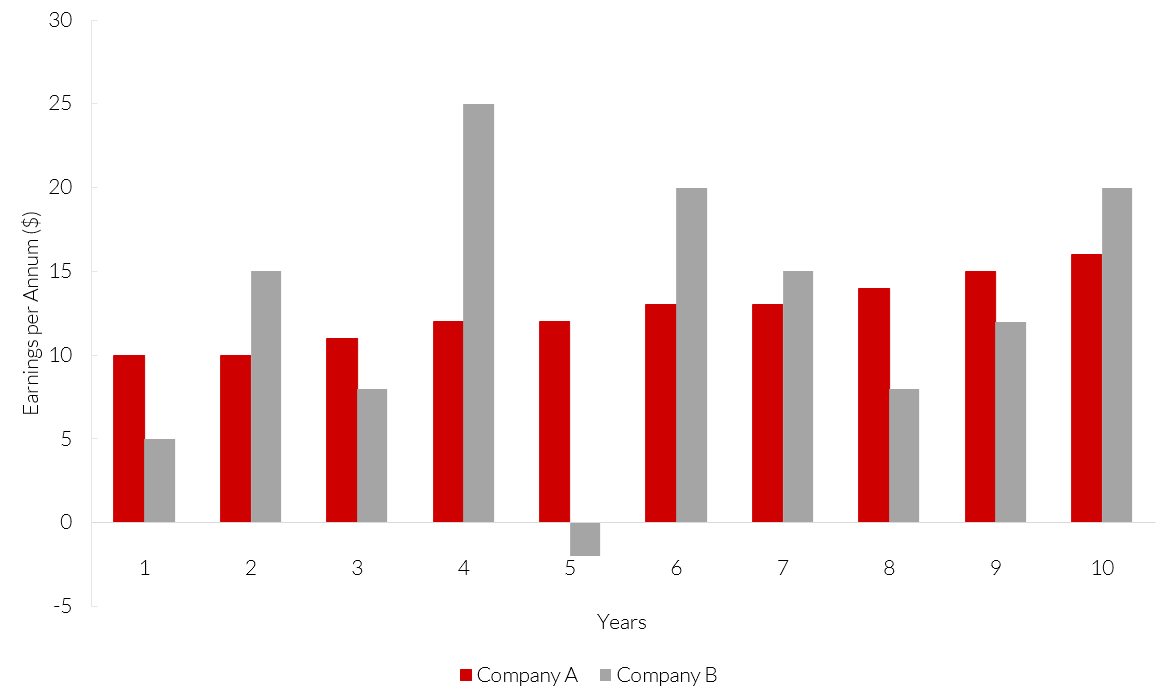

Take for example two hypothetical companies, Company A and Company B. Company A operates in a relatively stable environment with a history of reasonably predictable earnings. Company B operates in a less predictable environment with an erratic earnings history. Assume that the future expected earnings profiles of the two companies are as shown in Graph 1. Both companies are expected to earn $126 over the next 10 years. Company A’s earnings are expected to grow steadily at 5% per annum. Company B’s earnings are extremely volatile and appear to be quite random.

Graph 1: The earnings profiles of two hypothetical companies

Source: Allan Gray

If you ignore the time value of money, assume that future earnings from both companies are identical in magnitude, and only differ in terms of timing and predictability, investors should be indifferent as to whether they hold Company A or Company B if the price of the two companies is the same. However, the price of these two companies is never equal.

Investors are happy to pay more for certainty, even if the return is lower

Company A may attract a 15 times multiple of year one’s earnings or $150. The more volatile Company B may attract a lower multiple, say 10 times, or $50. Investors are generally happy to ‘pay up’ for certainty and try to avoid holding companies where the future is very uncertain. The return to investors will therefore be much higher for Company B than for Company A. Both earn $126 over the next 10 years, but Company B only costs $50 whereas Company A costs $150.

The price that you pay makes a significant difference to your return

Even if the premium for certainty never goes away, the impact that one’s entry price has on the internal rate of return (IRR) is significant. The IRR measures the compound annual rate of return of an investment. For example, let’s assume that, in year 10, Company A still sells for 15 times earnings and Company B for 10 times earnings. Company A would be worth $240 in year 10 (15 times $16) and Company B would be worth $200 (still a discount to Company A’s valuation). Without boring readers with the maths, an investment in Company A would result in an 11% IRR over this 10-year holding period (commendable in the context of what is sustainable and achievable). Company B, however, would deliver a 30% IRR.

If you pay for the predictable, you may miss an opportunity

If you rush to pay high multiples for seemingly stable and predictable company earnings, you can miss out on significant opportunities. In the example above, you could have bought Company B and earned a 30% return per annum over 10 years, but instead you bought Company A for an 11% per annum return. One may well do much worse than the Company A example above. There is rarely such a thing as a certain outcome and investors generally pay a higher multiple of earnings for perceived certainty. The reality is often very different to the outcomes predicted by an exuberant and overly confident analyst community.

Investors in Challenger Ltd were recently reminded of the danger of extrapolating past earnings into the future

In the five years from 2012, Challenger’s investors experienced consistent strong growth with pre-tax ‘normalised’ earnings increasing 9% per annum. Potential favourable retirement income reforms and the prospect of further success in Challenger’s financial adviser aligned distribution strategy boded well for future earnings. Between June 2012 and December 2017, Challenger’s share price increased over fourfold as investors baked in continued strong earnings growth far into the future. This has proven wildly optimistic. Whilst its annuity sales have continued to grow, the mix has favoured less profitable annuities and investment assets. In addition, management’s assessment of ‘normal’ investment returns achievable, and therefore ‘normalised’ earnings, has also proven to be optimistic. Declines in interest rates and credit spreads have also started to put pressure on Challenger’s earnings. The once ‘certain’ high single digit earnings growth each year has evaporated. Challenger’s reclassification from a Company A-type company (with consistent earnings growth) to a Company B-type company (with more erratic earnings) has been painful, with its share price falling by more than 50% since December 2017.

Benefitting from mispricing opportunities is not as easy as it sounds

It requires a long-term perspective, a contrarian approach to investing and one must recognise that the future is far less predictable and certain than consensus would have one believe. These are some of the attributes that form the very fabric of our investment strategy at Allan Gray.

Simon Mawhinney is the Managing Director and Chief Investment Officer at Allan Gray Australia. He holds a Bachelor of Business Science (First Class Honours) with majors in Finance and Business Strategy and a Postgraduate Diploma in Accounting (University of Cape Town). Simon qualified as a Chartered Accountant in 1998 and is a CFA Charterholder.