Recently companies that have grown their earnings and paid large dividends have been well rewarded. In this extract from the latest Quarterly Commentary, Chief Investment Officer Simon Mawhinney questions whether the way this has been achieved is sustainable.

Since 2009, the sharemarket has handsomely rewarded companies that have been able to grow their earnings and pay large dividends in the process. This is unsurprising. A company’s value today is simply the present value of all the future dividends that investors will receive from owning that company. The company’s ability to pay those dividends is a function of its earnings. Therefore earnings and dividends are critical to any fundamental investor’s assessment of company value.

The sharemarket’s insatiable appetite for companies with growing earnings and dividend streams has blinded many investors to the way in which this growth is delivered. Today’s low interest rate environment has led to companies funding a greater proportion of their assets with very low-cost debt and increasing the proportion of earnings paid out to shareholders in the form of dividends.

This method may be the easiest way to deliver the growth that the market desires, but it is arguably the least sustainable way. It creates a short-term sugar hit in the form of increased earnings and, in this market, an even higher share price (which in turn usually leads to higher executive remuneration, a convenient coincidence). The trade-off is potentially lower future earnings (should interest rates increase) and significantly higher business risk from elevated levels of debt.

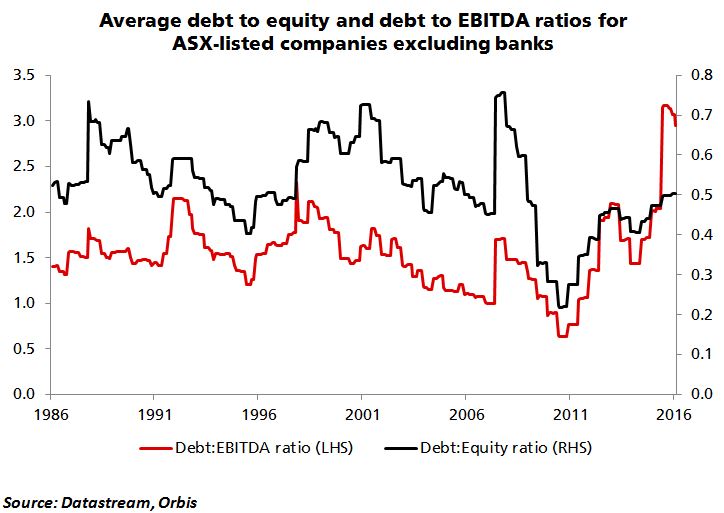

The chart shows the average debt to equity and debt to EBITDA (earnings before interest, tax, depreciation and amortisation) ratios for ASX-listed companies excluding banks (which are highly indebted). These metrics are widely accepted measures used to assess balance sheet strength.

Although current levels of gearing (as measured by the debt to equity ratio) are considerably below their all-time highs, they are well up on the lows of the last few years. The reduction in corporate earnings since 2011 (primarily from the resource-exposed companies) combined with this increased level of debt has contributed to the recent spike in the debt to EBITDA ratio. In both cases, the current trajectory is not sustainable and companies are becoming increasingly exposed to the potential threat of rising interest rates.

The current extended cycle of low interest rates has led to an element of complacency in assessing the business risks attached to elevated levels of company gearing. As a result, the attractiveness of lowly-geared companies appears to be underappreciated today. Some may consider our approach old-fashioned, but we’re much more attracted to companies whose management teams don’t rely on capital structure trickery to generate ‘increased’ value for shareholders.

You can read the full Quarterly Commentary here.

Simon Mawhinney holds a Bachelor of Business Science (First Class Honours) with majors in Finance and Business Strategy and a Postgraduate Diploma in Accounting (University of Cape Town). Simon qualified as a Chartered Accountant in 1998 and is a CFA Charterholder.

Simon

What are the numbers on each side? e.g. was EBITDA to debt 1.5 in 1986 and 3 now? Has debt:equity remained at about .5 from 1986 to 2016?

John Oxley CA(SA)

Hi John, yes it’s debt to EBITDA on the left-hand side which was roughly 1.5 in 1986 and roughly 3 now. Debt to Equity is shown on the right-hand side and although the number is roughly the same as it was 30 years ago, it has fluctuated significantly over that time. The point here is that the debt to equity ratio (company borrowings) is well up on the lows of the last few years, in an environment where debt relative to earnings has also risen strongly. It’s a real concern for us.