2016 was a great year for our investors, with performance bouncing back very strongly, but now is not a time for complacency. As the recent wave of initial public offerings shows, caution is critical. Chief Investment Officer Simon Mawhinney explains more in this extract from the latest Quarterly Commentary.

It has been a great year for our investors with performance bouncing back very strongly after a disappointing 2015. Readers may be pleased to know that, despite our recent success, we enter 2017 with the same razor-like focus and investment rigour as we entered 2016.

It has been a great year for our investors with performance bouncing back very strongly after a disappointing 2015. Readers may be pleased to know that, despite our recent success, we enter 2017 with the same razor-like focus and investment rigour as we entered 2016.

There is never a good time to be complacent when it comes to investing and we continue to scour the market for great opportunities. Exercising caution is critical and the recent Commentary wave of initial public offerings (IPOs) are a case in point.

IPOs are supposedly engineered to deliver good outcomes for investors and many remember the extreme success of the demutualisations and government sell-downs in the 1980s and 1990s. 2016, however, has been a particularly bad year for these newly-listed companies and the complacent investors who backed them. Not only have newly-listed companies been disproportionately represented in 2016’s corporate collapses, many of those that remain standing have significantly underperformed the broader sharemarket.

Dick Smith, Vocation and McAleese were all placed into administration recently with none of these managing to chalk up their three year anniversary as a listed company. Excluding these corporate failures, seven of the ten worst performing shares in the S&P ASX All Ordinaries Index this year were newly-listed companies. None of the best performing ten were newly-listed.

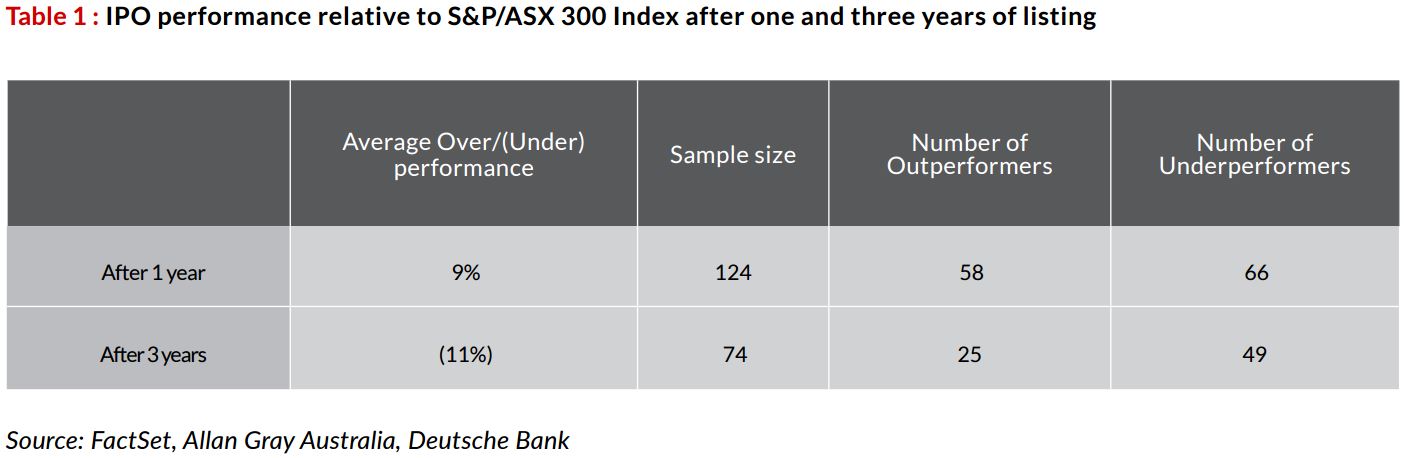

Picking on the worst performers is not necessarily representative of the entire sample of newly-listed companies. Over the past ten years, there have been 141 IPOs of Australian companies with market capitalisations of greater than $200m. Table 1 shows how these IPOs have performed relative to the broader sharemarket.

Of the 141 IPOs analysed, 124 have a track record greater than one year (i.e. 17 were listed in the past year). These companies have, on average, outperformed the sharemarket by 9% in their first year of trading. Extending the analysis to those with a three-or-more year track record reduces the sample size to 74. These companies have, on average, underperformed the sharemarket by 11%. In both categories there are more underperformers than outperformers.

This should not come as a surprise. IPOs today usually follow extremely favourable business conditions and are floated when the outlook is extremely optimistic. They are usually priced for perfection, with exiting shareholders eager to extract as high a price as possible. The greatest beneficiaries are the exiting founders or private equity shareholders, who know the most about their businesses, with fee-gouging investment banks close behind. These companies often outperform in their first year as a listed company but go on to significantly underperform the broader sharemarket when the cycle turns or their very optimistic projections reflected in the prospectus are not achieved.

It is for these reasons that we don’t typically participate in IPOs. Not only do we not have access to the same information as the sellers of these businesses, it is usually better to wait for less rosy outlooks to prevail, with resulting prices which more adequately compensate a buyer of shares for the risks they take on.

You can read the full Quarterly Commentary here.

Simon Mawhinney holds a Bachelor of Business Science (First Class Honours) with majors in Finance and Business Strategy and a Postgraduate Diploma in Accounting (University of Cape Town). Simon qualified as a Chartered Accountant in 1998 and is a CFA Charterholder.