In this extract from the December 2019 Quarterly Commentary Julian Morrison reviews the Allan Gray Australia Funds over the last quarter. Click here to read the full Quarterly Commentary.

Allan Gray Australia Equity Fund

The Australian sharemarket was up 0.7% for the fourth quarter, with a strong November keeping the broad market in positive territory, despite weakness at both the start and end of the period.

The Allan Gray Australia Equity Fund (Class A) underperformed its S&P/ASX 300 Accumulation Index benchmark by 1.2% for the last quarter, largely due to a weak month in October. The Class did recoup some of this, outperforming for the last two months of the quarter.

The largest detractor from performance for the quarter was Newcrest Mining, which was weak throughout the quarter. Another large factor in the underperformance was the absence of Healthcare exposure – a sector that continued to perform strongly, but where we continue to believe valuation risk remains high in general.

Positive contribution to performance came in the form of our underweight exposure to Financials, as well as stock selection within that sector. Our overweight exposure to Energy was also a positive factor, with Woodside Petroleum and Origin Energy both adding to relative performance. As 2020 begins with renewed global uncertainty, and the broad Australian sharemarket near all-time highs, we believe the value potential inherent in our energy, gold and other contrarian exposures remains significant.

Allan Gray Australia Balanced Fund

The Allan Gray Australia Balanced Fund outperformed its composite benchmark by 2% in the fourth quarter. The Fund has 68% in equities, though about 7% of the global share exposure is hedged, which allows for some protection in those periods where market indices fall. The Fund has been underweight Australian equities and overweight global equities. This bolstered relative performance for the quarter, as global equities outperformed Australian. In addition, stock selection in the global component further helped relative returns.

For the approximately 22% of the portfolio currently invested in fixed income, we remain significantly shorter in duration than the benchmark – at below two years versus seven for the benchmark. This has detracted from relative performance for some time in an environment of falling interest rates. However, the last quarter saw a slight reversal of this, with 10-year bond yields rising both in Australia and the US. This was a positive for the Fund, which remains more defensively positioned than the benchmark in terms of both relative and absolute returns, in the event interest rates rise.

Allan Gray Australia Stable Fund

The Allan Gray Australia Stable Fund outperformed its cash rate benchmark by 0.4% in the fourth quarter.

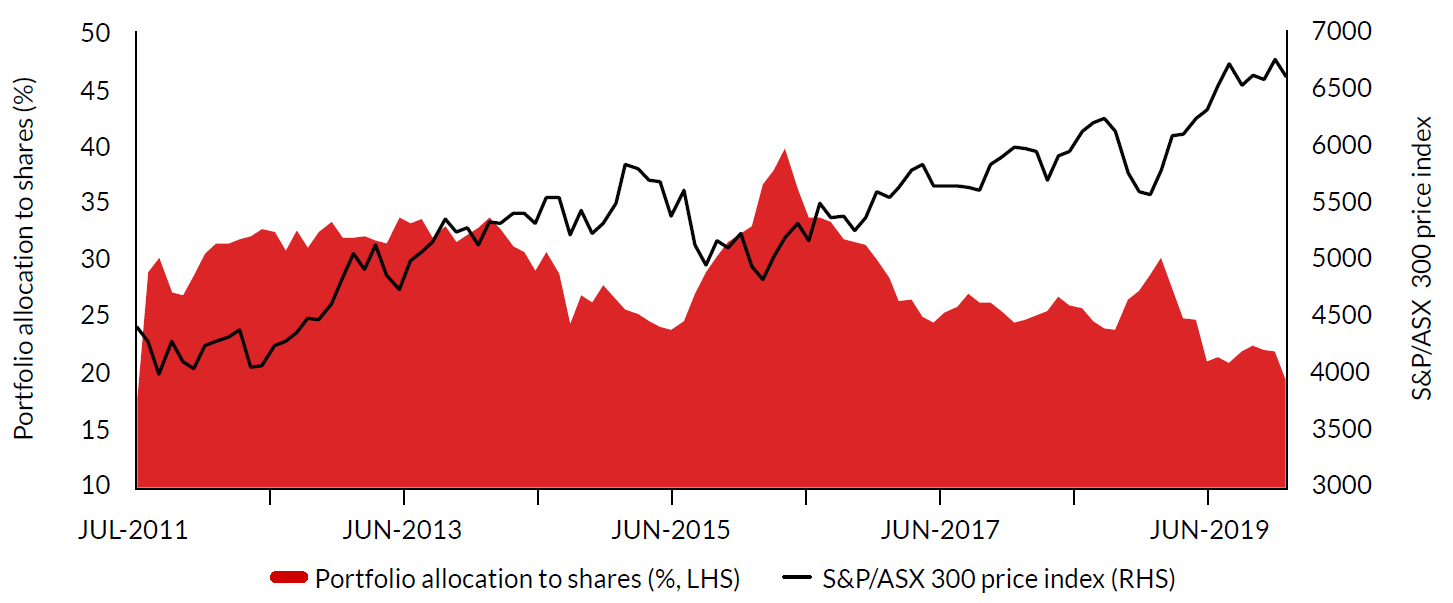

The performance of the Stable Fund is driven by the performance of our favoured Australian share holdings and the decision on how much of the portfolio is invested in shares versus cash. The exposure to shares can range from zero to 50% of the Fund and the allocation over time is illustrated in the red shaded area in Graph 3. As the sharemarket has risen strongly over the course of the last year, we have reduced the Fund’s overall exposure to shares. At the end of the fourth quarter, exposure to selected shares remains near the lowest in the history of the Fund at around 20%. We continue to focus these holdings in out-of-favour shares, such as Woodside Petroleum, Newcrest Mining and Sims Metal Management, where we believe the price is not reflective of their value and which therefore offer some defensive qualities in a potentially expensive overall market.

Stable Fund portfolio weightings – equity allocation falls when there is less value in equities

Source: Allan Gray as at 31 December 2019

Julian Morrison holds a Bachelor of Arts (Honours – University of Sheffield) and the Chartered Financial Analyst designation.