This post was co-written by two key members of the Allan Gray retail team, Werner du Preez, who is responsible for the distribution of the Allan Gray Australia funds in South Africa, and Chris Inifer, Head of Retail.

This post was co-written by two key members of the Allan Gray retail team, Werner du Preez, who is responsible for the distribution of the Allan Gray Australia funds in South Africa, and Chris Inifer, Head of Retail.

You probably know the Aesop Fable about an ant and a grasshopper. During summer, the sensible ant stores food for the winter while the grasshopper happily makes music. When winter comes the grasshopper is starving and begging the ant for food. The moral is that it is best to prepare for the days of necessity.

Can you picture the future?

If you can you’re better than most.

Unless we want a retirement spent in poverty it’s essential that we provide for our future. We all know that this is one of the most important things we need to do – when we no longer earn a salary we have to generate our cash flow from elsewhere – so why do we find it so difficult to do?

Unfortunately human nature plays a big part.

As humans we simply don’t have the inherent instinct to jolt us into the action required to prepare for our future. Most of us need to force ourselves to actively think and plan ahead to deal with the distant future. While we are easily concerned with immediate events and desires, we struggle to visualise our future in vivid terms and it’s very difficult for us to imagine where we will be in ten years from now.

What happens when you think of your future self?

A 2009 study conducted by Hal Hershfield at Stanford University measured the brain activity of participants while instructing them to think about three people:

a) themselves

b) a stranger

c) themselves ten years from then.

The study concluded that there are significant differences in our brain activity and how we feel when thinking about ourselves in the present, compared to imagining ourselves in the future.

For many of the participants, the areas and pattern that becomes activated in the brain for the future self is more like that of the stranger. Some people identify with their future self to some extent, but for many the ten-year older version of them might as well be a complete stranger. Evidently it is hard for us to place ourselves in our own shoes ten years from now.

Making sacrifices now to look after your future

It stands to reason that if we were able to feel greater identification and continuity with who we will become, we should find it easier to sacrifice more of our current pleasures for the sake of our future self.

Saving for retirement, or another long-term financial goal, is a good example. When just starting a career, we have to imagine a much older version of ourselves in order to set up the right savings plan to provide a comfortable retirement.

But typically most people do nothing. Ten years seems a long way away. If you can set up a savings plan, however, the rewards can really add up. With the power of compounding the investment can accumulate significant value.

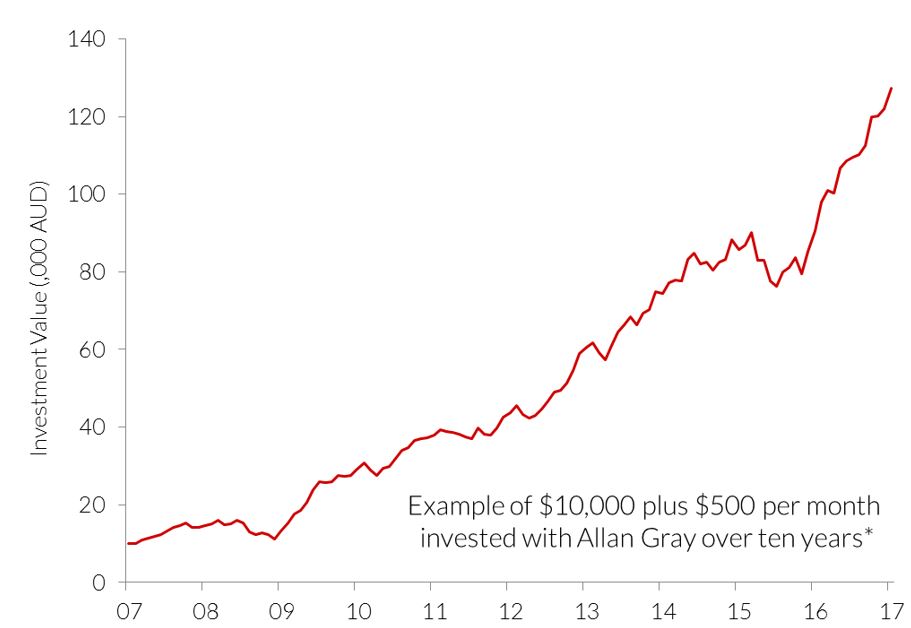

For example, if you had invested $10,000 in the Allan Gray Australia Equity Fund ten years ago, and then made a regular contribution of $500 per month for the next ten years, today that investment would be worth around $127,138.

Regular savings can really add up

If the ‘current you’ can adopt the right mindset to provide for the ‘future you’, we can share generously from what we currently give ourselves to what we allocate to ourselves in the future – remember this is your life you’re providing for, not a stranger’s. If we can’t adopt this mindset it’s likely that a large number of us will arrive at retirement with insufficient funds to maintain our lifestyles.

What can we do?

Most people are well aware that saving for the future and retirement is very important. But this knowledge often does not translate into appropriate behaviour. It’s difficult to inhibit our need for immediate gratification, even if we know we should, but there are ways to rectify the problem.

The following three strategies could help us to stick to our savings & investment plans in order to reach our goals:

1. Clearly define your objective (e.g. repaying the mortgage, paying school fees, or funding a retirement that maintains the lifestyle you’re accustomed to) and actively keep this chosen goal in mind

2. Monitor progress towards this goal and increase savings along the way if necessary

3. Reduce imprudent responses and reliance on willpower (e.g. by automating regular savings)

There will always be competition between our internal impulsive grasshopper and our sensible ant, with the grasshopper looking to live for the moment and the ant exerting discipline and self-control in pursuit of long-term goals. Careful evaluation of immediate rewards and consequences versus delayed rewards and the associated long-term benefits should help us to avoid finding ourselves as the hungry grasshopper knocking at the ant’s door when winter comes.

*Source: Allan Gray Australia, 30 April 2007 to 30 April 2017. Based on a $10,000 initial investment in Allan Gray Australia Equity Fund Class A units and $500 per month thereafter ($70,000 total contribution). Returns net of fees and assume reinvestment of distributions. Past performance is not a reliable indicator of future performance.

Chris Inifer holds a Bachelor of Business Economics and Finance (RMIT University) and a Postgraduate Diploma (with Distinction) in Financial Planning.

Werner du Preez joined Allan Gray South Africa in 2008. He is responsible for the distribution of the Allan Gray Australia funds in South Africa. He holds an M Com and is a CFP.