Investors can be seduced by forecasts of large growth in an industry. But as Simon Marais, one of Allan Gray Australia’s founders, has previously highlighted (in an article reprinted below), high growth in an industry often leads to disappointment for shareholders.

Two sectors that are growing rapidly in Australia today are the markets for vitamins and baby formula. Expectations for continued growth remain high, as both industries are benefitting from strong demand from Asian markets. However, our funds are not invested in any companies from these sectors because we see large risks.

The barriers to entry in these markets are relatively low; there is little to stop new competitors from coming in and making life difficult for the current firms. In our experience it’s often the case that as new entrants enter a sector and competition increases, then returns on capital often fall to more pedestrian levels.

That’s why we focus on bottom-up analysis; focusing our energy on underlying business fundamentals such as competitive position, return on capital and sensible management rather than industry growth rates and macroeconomic variables.

What Simon said in 2008 holds true today and serves as a timely reminder that fundamental analysis can help ensure we do not overpay for shares in popular sectors. You can read the original article below and post your comments.

The benefits (or not?) of foresight

This piece was originally published in 2008 and has been edited slightly for length. Simon Marais concludes that, even if we could forecast the future of industry growth, it is far from clear that it would be much help. Instead, investment decisions should be made by a detailed study of companies which other investors have written off because they dislike the industry or find it ‘boring’.

At Allan Gray we do not usually have colourful charts to show clients about growth in China or the latest sub-prime disaster in America. The reason for this is simple – most of the time we have no special knowledge about such affairs and therefore cannot add to what is already known in the market.

But there is an even deeper reason for trying to limit our reliance on economic forecasting. Suppose you had perfect knowledge about which sector would experience the best growth over the next 30 years and which the least. Surely this would make your investment decisions easy? Buy the best industry and avoid the worst.

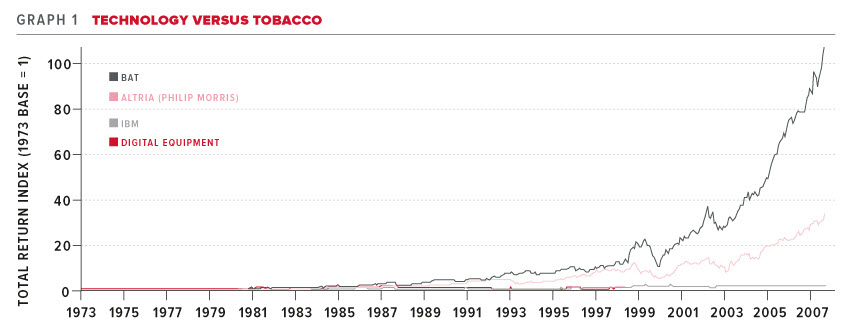

Which sector has shown the best growth since 1973 and which has experienced the most headwinds?

Looking at our Orbis database which goes back to 1973, we conclude that developments in the information technology (IT) sector have exceeded even the highest expectations of 35 years ago. Meanwhile, the worst performing industry since then has probably been tobacco. In 1973, smoking was still common on aeroplanes and you would probably have been classified as eccentric if you had told someone to smoke outside.

Armed with this knowledge, you would think making money (at least in a relative sense) would be simple: buy the dominant companies in the IT sector and stay away from tobacco companies. Back then, IBM dominated the computer space, while the largest tobacco company was Phillip Morris (now called Altria).

Graph 1 shows the value of an investment in 1973 in both stocks with dividends re-invested. A US$100 investment in IBM had grown to US$1,700 by the end of 2007 – a little better than inflation, but worse than the general stock market which yielded US$3,500. Foresight on the IT sector would have been of no help. But an investment in Phillip Morris/Altria increased to US$35,000 over the same period – 20 times more than the IBM investment and 10 times more than the stock market.

Source: Datastream

Where there is smoke there is fire

Our choice of companies was not just fortunate. The second-largest computer company of the day was Digital Equipment, which was taken over by Compaq 10 years ago for less than four times its 1973 price. You have to look carefully to distinguish Digital Equipment’s graph from the bottom axis. Meanwhile, British American Tobacco (BAT), the second-largest tobacco company at the time, was up 1,000 times.

The importance of a holistic approach to financial markets research

The examples mentioned illustrate that perfect foresight in macroeconomics is often of little value; in fact, it could actively lead you to make poor investments. One of the most underappreciated facts about financial market research is, in our view, that it is not only the growth in your markets that is important; even more significant is the growth in competition that you face. This is the part that is very difficult, if not impossible, to predict.

The computer industry experienced rapid growth, but that spawned massive competition and constant innovation. The large incumbents of the day had to fight both existing and new competitors for their market. Emerging competitors such as Apple, Microsoft, Dell and Google had innovative business models that the incumbents found difficult to copy. At the same time, the tobacco industry faced a shrinking market, rising taxes, a ban on advertising and a series of huge lawsuits.

However, nobody entered the market and the incumbents could pass all costs on to their customers and, with no re-investment needs, all profits could flow to investors as dividends.

Cracks in the crystal ball theory

So we can conclude that even if (and it is a very big if) we could forecast the future of industry growth, it is far from clear whether the information would help much. Instead, we elect to stick to our investment philosophy: we make our investment decisions by completing a detailed study of companies. We often choose industries that other investors dislike or have written off as ‘boring’. Our research involves a careful study of financial accounts and annual reports, management and competitor interviews and a strong focus on value. In this way we make sure we do not overpay.

While this approach does not work every year (as some of our more recent numbers show), it has stood us in good stead since inception. We have no doubt that as long as we keep up our standards of analysis, our approach will work for the next 34 years.

No need for that crystal ball then!

Chris Inifer holds a Bachelor of Business Economics and Finance (RMIT University) and a Postgraduate Diploma (with Distinction) in Financial Planning.