Finding a quality manager can be tricky for any investor. With so many funds, it can be very difficult to know where to start. In this post, we highlight two measures that may provide a starting point to narrow the list when selecting an active manager.

In a 2014 paper, authors Matijn Cremers and Ankur Pareek grouped mutual funds according to ‘active share’ and ‘turnover’ as two indicators of long-term outperformance potential. The study found that high active share combined with low turnover was a strong indicator for potential outperformance.

Look for a high active share – deviating from the benchmark can be rewarding‘

Active share’ measures the extent to which a fund’s holdings differ from the benchmark’s holdings. You can learn more about the importance of active share in L.J. Collyer’s recent post. But in simple terms, a fund with a high percentage active share would differ significantly from the benchmark where a lower percentage would be considered a less active or even a ‘closet index’ fund. By definition, the potential for outperformance requires substantially different positioning relative to the benchmark.

Maintain low fund turnover – why patience pays

The paper goes on to identify that even with a high active share, funds that trade frequently generally struggle to outperform. So, it is a combination of high active share and low turnover that led to significant outperformance over time.Fund turnover measures how frequently the manager trades assets in the underlying portfolio and in turn the average length of time that an asset is held.

Funds with low turnover can outperform funds with high turnover for two reasons:

1. High-turnover funds spend more on trading commissions, which are a significant fund expense.

2. Increased trading by high-turnover funds means the manager needs to make the right investment decision more frequently, as mistakes can be costly.

High turnover can demonstrate a lack of belief in investment ideas on the fund manager’s part and the tendency to overreact to short-term market movements. Low turnover requires strong manager conviction that holdings can deliver and offers greater potential for long-term outperformance.

Combining these strategies offers the most potential outperformance

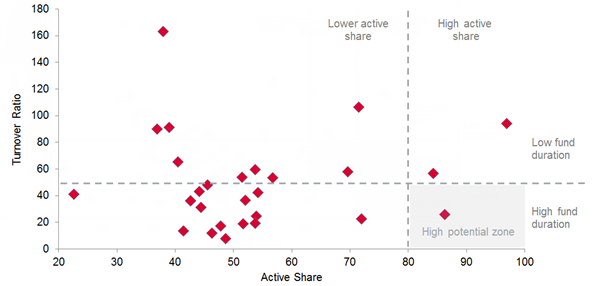

With this in mind, the chart below shows all Australian equity managers with a large cap benchmark and a fund size that is greater than $100 million that provide turnover and active share data to Morningstar.

High active share and low turnover reveals the high potential performance zone

Source: Morningstar data and 2014 paper by Cremers and Pareek

Active share is on the horizontal axis and turnover is on the vertical axis. Identified on the graph are lower active share, high active share, low fund duration and high fund duration. The two measures help identify which funds are truly active, and which have the potential to benefit from their patience. The area to focus your attention is the ‘high potential zone’. According to the 2014 paper by Cremers and Pareek, this is the area that gives managers the potential to achieve the greatest outperformance.

One fund that stood out in the sample was the Allan Gray Australia Equity Fund with a high active share and a low turnover. But there weren’t many other managers that fit within this range. In the Australian market this outcome suggests that managers may be avoiding the high potential zone of high active share and low turnover.

Why would managers avoid the high potential performance zone?

As Jeremy Grantham of the global investment firm GMO commented, the central truth of the investment business is that career risk can drive investment behaviour. People are generally afraid of being wrong on their own. To prevent this, professional investors tend to pay a lot of attention to what their peers are doing. The great majority ‘go with the flow’ and it creates herding, or momentum, which drives prices far above or far below fair price. There are many other inefficiencies in market pricing, but this is by far the largest.

Patience is a virtue, for fund managers and investors

Warren Buffett has commented that the share market is a mechanism that transfers wealth from the impatient to the patient. The point is that even if you select a better-than-average manager, you should expect to experience periods of meaningful underperformance. And you will need fortitude and patience to benefit fully from the outperformance the manager may deliver over time.

Conviction and patience are not skills on their own

At Allan Gray we believe in being truly contrarian. This means doing things differently. We believe in a long-term, fundamental approach which means thinking like a business owner instead of a stock trader. The skill lies in the manager’s ability to value businesses accurately, which we acknowledge is not easy to do, and success depends on whether the organisation has the patience to allow conviction in unpopular ideas.

Joy Yacoub holds a Bachelor of Economics and a Bachelor of Commerce (UNSW), specialising in Economics, Finance and Business law.