In January this year, my partner told me that she’d been doing her research and she planned to start investing. Her interest had been piqued as I had been selfishly boring her with long explanations of Allan Gray’s history, our contrarian approach and how our philosophy translates to uncovering market opportunities. Faced with frequent reminders from her bank that the interest earned in her savings account was once again to fall, and seeing the impact of a decade-long bull market in equities, she was ready to begin. I encouraged my partner to look at all her options and to consider getting financial advice.

In January this year, my partner told me that she’d been doing her research and she planned to start investing. Her interest had been piqued as I had been selfishly boring her with long explanations of Allan Gray’s history, our contrarian approach and how our philosophy translates to uncovering market opportunities. Faced with frequent reminders from her bank that the interest earned in her savings account was once again to fall, and seeing the impact of a decade-long bull market in equities, she was ready to begin. I encouraged my partner to look at all her options and to consider getting financial advice.

Even armed with all this, she was quite nervous and I understood and shared her concerns. Investing in anything, let alone equities, exposes investors to both upside and downside risks. No matter how much research and preparation one does before taking the plunge, seeing the value of your hard-earned cash rising and falling can be a very jarring experience.

Compounding our nervousness was the fact that the sharemarket in aggregate looked expensive. With domestic price to earnings ratios far above long-term averages, the prospects for the high returns we had experienced over the past decade to continue into the future seemed dimmer, and the risks appeared heightened.

Horses for courses

A common way investors significantly impair their capital is by being positioned too far out along the risk curve, then selling their holdings toward the bottom of an asset price fall that was too much for them to stomach. An event like this can turn someone off investing altogether, robbing them of the enormous potential benefits of compounding returns for the rest of their lives.

My partner worried how she would feel if she was to experience a major market crash. If something like this happened, would she stay the course and dutifully refuse to look at her account balance until things had improved? Would she fight against her instincts and human nature and allocate more capital as others ran for the exits? Or would she panic, and sell at the worst possible time?

She feared it could be the latter of these three, as she was acutely aware of her own risk tolerance in day-to-day life. Having read up on a range of available funds, she decided she would start by investing in the Allan Gray Australia Stable Fund. Her rationale was that this would allow her to get used to seeing some degree of the daily fluctuations of equity markets and continue to learn more about investing (her reading has since progressed from Scott Pape to Benjamin Graham).

The Stable Fund is predominantly invested in cash, but aims to outperform the RBA cash rate by investing no more than 50% of its portfolio in the Australian sharemarket as attractive opportunities present themselves. The level of equity exposure is not the result of a macroeconomic, top down view on the likely direction of markets, but the bottom-up result of individually researched stocks under our contrarian, fundamental and long-term investment strategy.

How the Stable Fund works

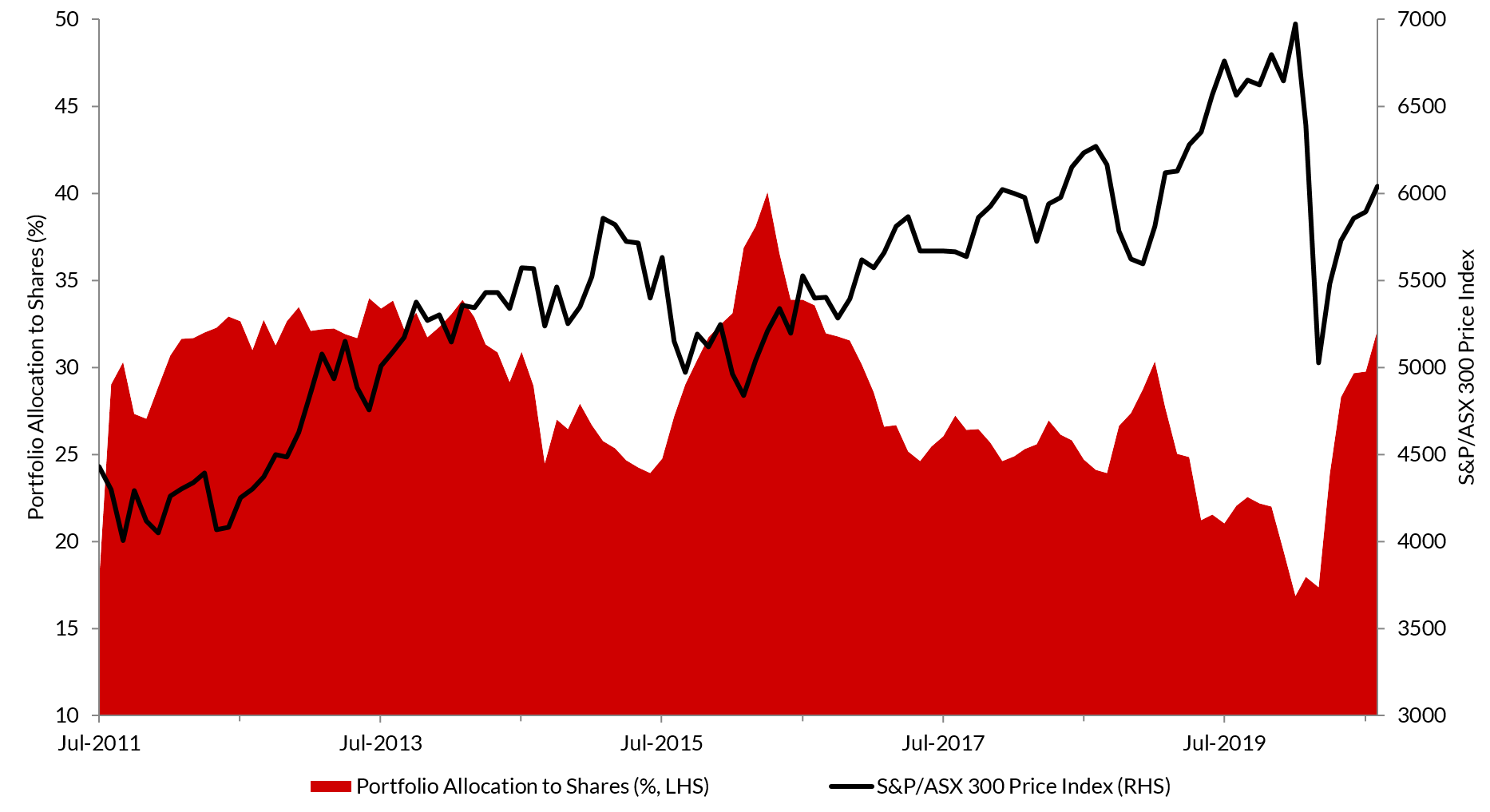

Since its inception in 2011, the Fund has had an average equity exposure of 28.4%, but this level has varied widely. Generally, when markets rise and price to earnings ratios expand, fewer stocks are far enough away from our assessment of intrinsic value to warrant their inclusion in this Fund, leading overall equity exposure to fall. When markets fall, the Fund naturally increases its share exposure as better value emerges.

This has once again occurred, with the COVID-19 volatility providing Allan Gray the opportunity to increase the Fund’s exposure from a record low of 15.5% in equities in March to now having over 32% exposure to equities as at 31 August 2020. You can see how the exposure to equities has fluctuated as the sharemarket rises and falls in Graph 1.

Graph 1: Stable Fund portfolio weightings – share allocation rises where we see value in shares

Source: Allan Gray Australia, Bloomberg, as at 31 August 2020, inception 1 July 2011.

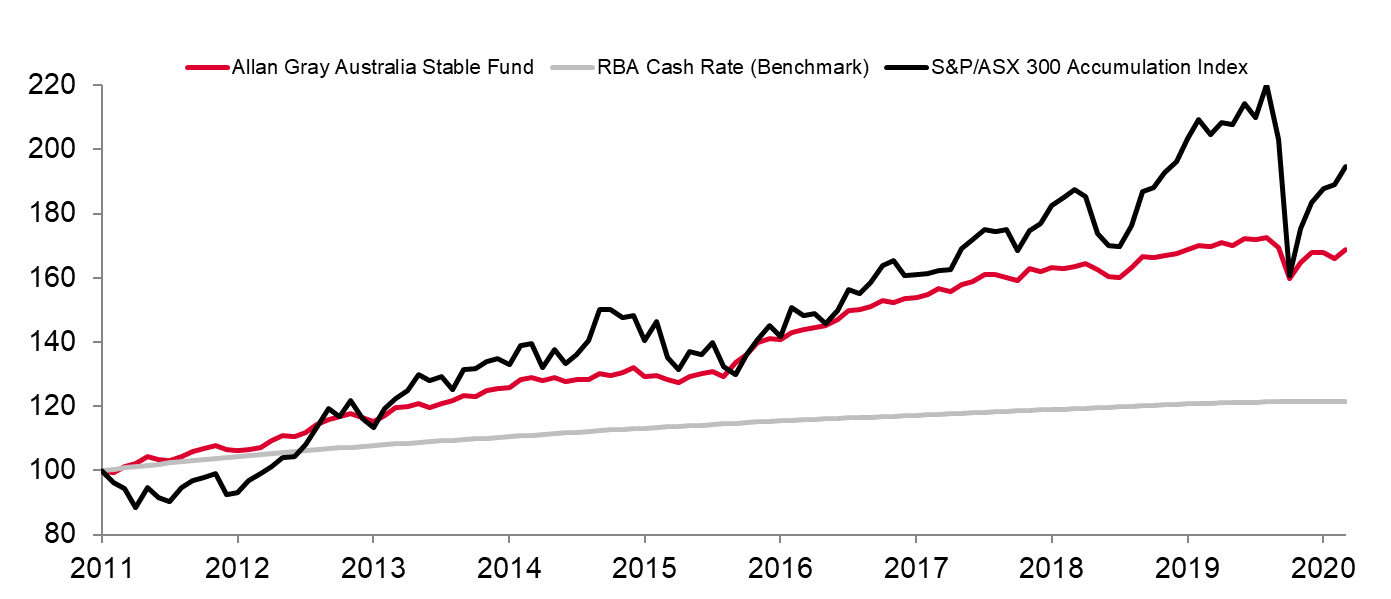

The Fund’s ability to adjust its exposure to equities has led to a much smoother return profile over time, compared to the Australian sharemarket (as seen in Graph 2). At one point during the recent crash, the Fund had provided the same total return as the S&P/ASX 300 Accumulation Index since its inception, with less than a third of the average equity exposure taken on by the investor.

Graph 2: The Stable Fund has delivered a smoother return profile than the Australian sharemarket

Source: Allan Gray Australia as at 31 August 2020. Past performance is not indicative of future performance.

My partner’s timing in entering markets turned out to be very unfortunate, but she is investing for the long term. Trying to time entry into markets is a fool’s errand and hindsight always comes with 20/20 vision. Thankfully, her decision to start her investing journey with the Stable Fund has allowed her to experience a less severe rollercoaster ride to date, which she feels is right for her.

For someone like my partner, a more conservative investor looking to outperform the low rates on offer for cash and able to weather some ups and downs, the Stable Fund may offer a simple and unique alternative.

Chris joined Allan Gray in 2019 as a Research Associate, before moving into the Relationship Manager role in 2020. Prior to joining Allan Gray, Chris worked at BT Financial Group from 2014 to 2019, where he held a number of management roles across the Insurance and Superannuation businesses.